The Mortgage Rates Hit New Low of 3.89%! Will Rates Go Down Further In 2019?

Posted by: Connie in Interest Rates

New Zealand Reserve Bank (RBNZ) cut the official cash rate (OCR) from 1.75% to 1.5% on 8th May 2019. The 1.5% OCR is a new record low. As a result, New Zealand major banks, ANZ, BNZ, Westpac and ASB have cut mortgage rates after RBNZ decision to drop OCR. So, how long should I fix my mortgage for 2019? Will New Zealand mortgage rates go down further in 2019?

The Mortgage Rates Hit New Low (3.89%)!

Will Home Loan Rates Go Down Further In 2019?

Video Timeline:

1. May 2019 Mortgage rates update – hit the lowest in New Zealand interest rate history – 00:44

2. Will New Zealand mortgage rates go down further in 2019? – 02:38

3. How long should I fix my mortgage for 2019? – 03:23

1. May 2019 Mortgage rates update – hit the lowest in New Zealand interest rate history

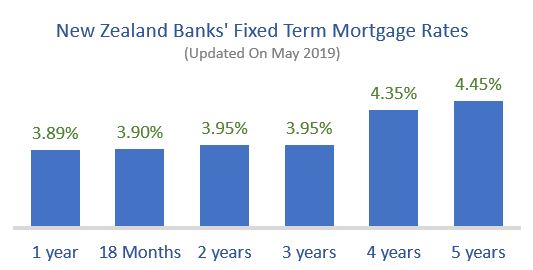

The current one-year fixed term mortgage rates of 3.89% hit the lowest in New Zealand interest rate history. It’s the best home loan interest rates ever. Two- and three-year fixed term rates are the second best. The long-term fixed rates are still over 4%.

It’s worth mentioning that the above special mortgage rates may not apply to all New Zealand banks. For example, ANZ and Westpac offer one-year fixed term rate of 3.89% while ASB home loan rates of one year are 3.95%.

Also, some New Zealand banks, BNZ for example, offer higher rates to investment loan than residential owner occupied. This is because lending for residential investment property generally carries a higher cost for banks compared with lending for owner occupied properties. They choose to pass on their additional cost to customers.

2. Will New Zealand mortgage rates go down further in 2019?

The answer is: it depends on the OCR announcement that will be published by the New Zealand Reserve Bank at the end of 2019.

Some economists predict that the New Zealand Reserve Bank would decrease OCR at the end of 2019. What does this mean for your mortgage rate? New Zealand banks should decrease the mortgage rates further as supposed. However, RBNZ may require New Zealand banks to hold more capital, which will lead to the increasing of the lending costs. If they choose to pass their additional costs to their customers, then the supposed cut of mortgage rates will be offset by the cost increase. Therefore, the interest rates will be slightly lower or no change.

3. How long should I fix my mortgage for 2019?

Should you re-fix your loan to a one or two-year fixed term with lower interest rates or longer term? The answer is: it depends.

In what situation should you choose a short-term fixed rate?

If you do not expect your family net income will decrease in next two years, we highly recommend that you should take advantage of this special rates and fix your mortgage within two years. This will allow you to re-fix your mortgage with potential better rates should the interest rates drop further in the near future. Also, if you decide to break your loan, the break costs for short-term fixed loan are more likely less than four- or five-year fixed loan.

It’s worth mentioning that fixing mortgage with the lowest rate is not always the best decision for each case because in some situation, you might need to increase the certainty and minimise the risk of increased loan repayment.

So, in what situation should you choose a medium- or long-term fixed rate?

For instance, if you have a large amount of loan, one million for example, you might need to consider fixing some part of your loan with a long-term period. Just in case if the interest rates go up in the future, then it will help you to minimise the risk of increased loan repayment. This is because this strategy will allow you some time to prepare if the interest rate goes up in the future or if you experience financial difficulties.

What’s more, if you plan to have a baby, start a business, change your full-time job to part-time, or any cases that will have an impact on decreasing your family net income in next two years, we highly recommend you to fix your mortgage with longer terms.

Disclaimer: The content in this article are provided for general situation purpose only. To the extent that any such information, opinions, views and recommendations constitute advice, they do not take into account any person’s particular financial situation or goals and, accordingly, do not constitute personalised financial advice. We therefore recommend that you seek advice from your adviser before taking any action.

Get in touch

To get your personalised mortgage plan sorted and to secure the best mortgage rate for you, get in touch with us today by calling 09 930 8999 or emailing: support@profin.co.nz

If you are interested in taking advantage of the special rates, our experienced advisor will help you balance the benefits of securing a lower interest rate and ensure that the benefits outweigh the potential costs. We are happy to help you review your loan and find the best solutions for you.

Other Blogs That You Might Like:

Why should you consider refinancing your mortgage?

Should I re-fix my mortgage now or wait for my fixed term to expire?

All you need to know about New Zealand’s ring-fencing of residential rental losses bill

New Zealand Reserve Bank (RBNZ) cut the official cash rate (OCR) from 1.75% to 1.5% on 8th May 2019. The 1.5% OCR is a new record low. As a result, New Zealand major banks, ANZ, BNZ, Westpac and ASB have cut mortgage rates after RBNZ decision to drop OCR. So, how long should I fix my mortgage for 2019? Will New Zealand mortgage rates go down further in 2019?

The Mortgage Rates Hit New Low (3.89%)!

Will Home Loan Rates Go Down Further In 2019?

Video Timeline:

1. May 2019 Mortgage rates update – hit the lowest in New Zealand interest rate history – 00:44

2. Will New Zealand mortgage rates go down further in 2019? – 02:38

3. How long should I fix my mortgage for 2019? – 03:23

1. May 2019 Mortgage rates update – hit the lowest in New Zealand interest rate history

The current one-year fixed term mortgage rates of 3.89% hit the lowest in New Zealand interest rate history. It’s the best home loan interest rates ever. Two- and three-year fixed term rates are the second best. The long-term fixed rates are still over 4%.

It’s worth mentioning that the above special mortgage rates may not apply to all New Zealand banks. For example, ANZ and Westpac offer one-year fixed term rate of 3.89% while ASB home loan rates of one year are 3.95%.

Also, some New Zealand banks, BNZ for example, offer higher rates to investment loan than residential owner occupied. This is because lending for residential investment property generally carries a higher cost for banks compared with lending for owner occupied properties. They choose to pass on their additional cost to customers.

2. Will New Zealand mortgage rates go down further in 2019?

The answer is: it depends on the OCR announcement that will be published by the New Zealand Reserve Bank at the end of 2019.

Some economists predict that the New Zealand Reserve Bank would decrease OCR at the end of 2019. What does this mean for your mortgage rate? New Zealand banks should decrease the mortgage rates further as supposed. However, RBNZ may require New Zealand banks to hold more capital, which will lead to the increasing of the lending costs. If they choose to pass their additional costs to their customers, then the supposed cut of mortgage rates will be offset by the cost increase. Therefore, the interest rates will be slightly lower or no change.

3. How long should I fix my mortgage for 2019?

Should you re-fix your loan to a one or two-year fixed term with lower interest rates or longer term? The answer is: it depends.

In what situation should you choose a short-term fixed rate?

If you do not expect your family net income will decrease in next two years, we highly recommend that you should take advantage of this special rates and fix your mortgage within two years. This will allow you to re-fix your mortgage with potential better rates should the interest rates drop further in the near future. Also, if you decide to break your loan, the break costs for short-term fixed loan are more likely less than four- or five-year fixed loan.

It’s worth mentioning that fixing mortgage with the lowest rate is not always the best decision for each case because in some situation, you might need to increase the certainty and minimise the risk of increased loan repayment.

So, in what situation should you choose a medium- or long-term fixed rate?

For instance, if you have a large amount of loan, one million for example, you might need to consider fixing some part of your loan with a long-term period. Just in case if the interest rates go up in the future, then it will help you to minimise the risk of increased loan repayment. This is because this strategy will allow you some time to prepare if the interest rate goes up in the future or if you experience financial difficulties.

What’s more, if you plan to have a baby, start a business, change your full-time job to part-time, or any cases that will have an impact on decreasing your family net income in next two years, we highly recommend you to fix your mortgage with longer terms.

Disclaimer: The content in this article are provided for general situation purpose only. To the extent that any such information, opinions, views and recommendations constitute advice, they do not take into account any person’s particular financial situation or goals and, accordingly, do not constitute personalised financial advice. We therefore recommend that you seek advice from your adviser before taking any action.

Get in touch

To get your personalised mortgage plan sorted and to secure the best mortgage rate for you, get in touch with us today by calling 09 930 8999 or emailing: support@profin.co.nz

If you are interested in taking advantage of the special rates, our experienced advisor will help you balance the benefits of securing a lower interest rate and ensure that the benefits outweigh the potential costs. We are happy to help you review your loan and find the best solutions for you.

Other Blogs That You Might Like:

Why should you consider refinancing your mortgage?

Should I re-fix my mortgage now or wait for my fixed term to expire?

All you need to know about New Zealand’s ring-fencing of residential rental losses bill

Archive

- April 2026 (1)

- February 2026 (1)

- December 2025 (1)

- October 2025 (1)

- August 2025 (2)

- July 2025 (1)

- June 2025 (2)

- April 2025 (1)

- October 2024 (1)

- July 2024 (1)

- June 2024 (1)

- April 2024 (1)

- January 2024 (1)

- December 2023 (1)

- November 2023 (3)

- October 2023 (3)

- September 2023 (3)

- August 2023 (2)

- July 2023 (4)

- June 2023 (2)

- May 2023 (5)

- April 2023 (4)

- March 2023 (2)

- February 2023 (3)

- November 2022 (4)

- October 2022 (1)

- September 2022 (2)

- August 2022 (1)

- July 2022 (4)

- June 2022 (2)

- April 2022 (1)

- March 2022 (3)

- February 2022 (1)

- December 2021 (3)

- November 2021 (3)

- October 2021 (3)

- September 2021 (3)

- August 2021 (2)

- July 2021 (2)

- June 2021 (2)

- May 2021 (3)

- April 2021 (3)

- March 2021 (3)

- February 2021 (4)

- January 2021 (3)

- December 2020 (3)

- November 2020 (4)

- October 2020 (3)

- September 2020 (2)

- August 2020 (2)

- July 2020 (5)

- June 2020 (3)

- May 2020 (3)

- April 2020 (4)

- March 2020 (4)

- February 2020 (3)

- January 2020 (3)

- December 2019 (1)

- November 2019 (4)

- October 2019 (5)

- September 2019 (4)

- August 2019 (4)

- July 2019 (5)

- June 2019 (4)

- May 2019 (5)

- April 2019 (3)

- March 2019 (5)

- February 2019 (3)

- January 2019 (1)

- November 2018 (1)

- October 2018 (1)

- January 2018 (4)