What should you do when your interest-only mortgage ends within the next two years?

Posted by: Connie in Property Investing

When it comes to buying a house, an interest-only loan can be an attractive option. “Interest-only” means that the borrower only needs to pay the interest owing on their loan when they make a mortgage payment. This is a way to reduce mortgage payments and works well for investors, especially when their home loan hasn’t been paid off yet.

What are the benefits of an interest-only loan? For one, investors can enjoy the lower monthly mortgage repayments and have more cash available to repay other loans. Secondly, interest only loans also give investors more control over their cash flow, by allowing them to keep their costs down and claim tax against their investment property.

Currently, interest-only mortgage loans are only available for up to a five-year fixed term. Whereas, in the last few years, the fixed term that borrowers could apply for an interest-only loan was up to 10 or 15 years.

Let’s look at an example of when an interest-only loan is due to end soon. You may have some investment properties with a combined remaining loan amount of $1.5 million. You are only paying interest on these loans now and the fixed term is ending soon. The default option is to move to a principal and interest loan, but you are worried that your current family net income is insufficient to cover the higher repayments. So, you might be wondering if you can get an extension on your interest-only mortgage.

So, the question is:

What should you do when your interest-only mortgage ends within two years?

Video Timeline

1. How does an interest-only loan vs a principal and interest loan affect your cash flow? - 00:07

2. What are your options when your interest-only mortgage is ending soon? - 03:00

1. How does an interest-only loan vs a principal and interest loan affect your cash flow?

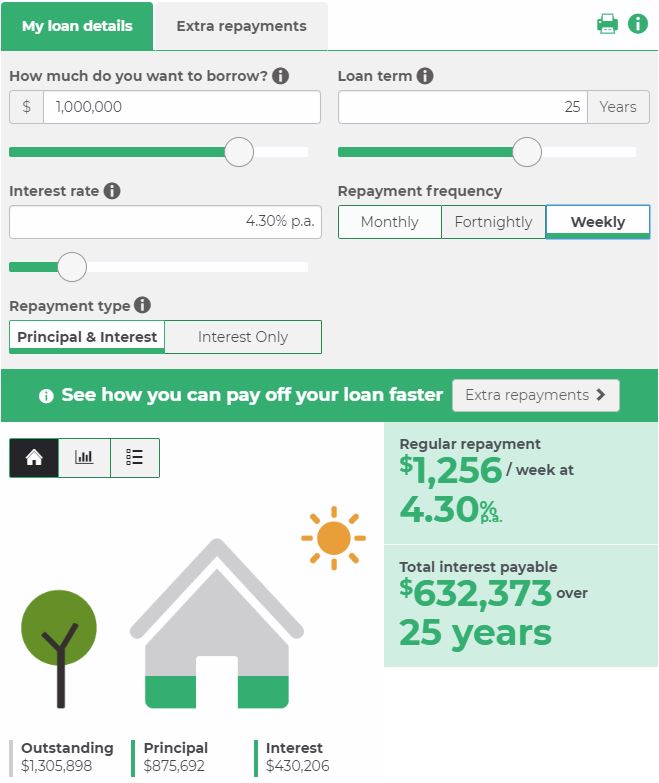

Based on a 25-year loan of $1 million with a 4.3% interest-only mortgage rate, the required weekly payment is $865. In contrast, borrowers who have a principal and interest loan for the same loan amount would have to pay a total of $1,256 weekly. This equates to a difference of $391 between the two repayment options.

When your interest-only term is about to end, your lender will automatically switch you to a principal and interest loan. From the above interest-only loan example, we know the loan repayment will rise. It could be risky for you if you have insufficient cash flow to pay the mortgage.

Faced with the risk of insufficient cash flow when the interest-only term on your mortgage ends, you might consider increasing your rental fee on your investment properties. However, it seems unlikely that you can get an additional $400 (rounded-up) from your tenants. You also have the option to increase your job income to get more cash flow. But, on the whole, it’s not easy to get an additional $400 cash flow from an increase in your rental or job income.

If you are wondering how to calculate your interest-only loan repayments, you can check our handy mortgage calculator. By simply typing in your loan amount, loan term and current fixed interest rate, you will know exactly how much more principal and interest you will pay after your interest-only period ends.

Here’s the link for our mortgage calculator: http://prosperityfinance.co.nz/calculators

2. What are your options when your interest-only mortgage is ending soon?

What happens when interest only loan expires?

Our customers often ask us what they can do when they reach the end of an interest-only mortgage term. There are usually several options they can choose from.

Option 1: Get an interest-only extension from your existing lender

You can ask your current lender if it’s possible to extend your interest-only mortgage term to give you more time to pay it off.

Your lenders might need to check your current personal income and family situation, so that they can evaluate your ability to repay the mortgage over a longer period. Also, New Zealand bank policies are becoming a lot more conservative, which means there is no guarantee that you will get your interest-only loan extension approved by your current lender. Therefore, if you can’t prove that you have adequate income to cover the repayments, you might struggle to convince your lender to extend your term.

Option 2: Refinance your mortgage to another interest-only loan

If your current lender doesn’t extend the term of your interest-only loan, another option is to refinance to an interest-only loan with a different lender. You can continue to make interest-only repayments for another five years and keep your costs on your investment property down.

It all comes down to policy at a particular bank. Failing to get an interest-only loan extension approved from your current lender doesn’t necessarily mean that you can’t get approval from another bank.

Prosperity Finance enjoys a good relationship with many New Zealand lenders, which allows us to search through many home loan options and find the right lenders to suit your personal situation and needs.

When we review your loan and help you refinance your mortgage, Prosperity Finance can also help you secure other benefits, including improving your loan structure to protect your asset, reducing your loan interest and helping you pay off your loan faster.

Option 3: Start paying the principal and interest (P&I) with your current lender

What happens if neither an interest-only extension from your existing lender nor refinancing your mortgage to another interest-only loan suits you? In this case, your current lender will automatically switch you to a principal and interest loan when your interest-only loan term ends. This option might not be a bad idea – as you can start repaying the loan principal and interest if you have adequate cash flow to cover the repayments.

Option 4: Review your property portfolio

If the above three options are not available to you, you might need to consider other strategies when your interest-only mortgage expires, or is due to expire within the next two years.

Selling or downsizing your investment properties could help you reduce your loan repayments if you can’t afford it. You might make some money from the property sale and prevent ruining your credit score if your house prices have increased.

Disclaimer: The content in this article are provided for general situation purpose only. To the extent that any such information, opinions, views and recommendations constitute advice, they do not take into account any person’s particular financial situation or goals and, accordingly, do not constitute personalised financial advice. We therefore recommend that you seek advice from your adviser before taking any action.

Prosperity Finance - Here to help

Prosperity Finance looks at property investment strategically, empowering you to make the best long-term, informed decisions. We are professional mortgage brokers and are here to help. If your interest-only mortgage ends within the next two years, give us a call on 09 930 8999.

Other Blogs You Might Like:

Should I still refinance my mortgage even if my current rates are good?

Why should you consider refinancing your mortgage?

When it comes to buying a house, an interest-only loan can be an attractive option. “Interest-only” means that the borrower only needs to pay the interest owing on their loan when they make a mortgage payment. This is a way to reduce mortgage payments and works well for investors, especially when their home loan hasn’t been paid off yet.

What are the benefits of an interest-only loan? For one, investors can enjoy the lower monthly mortgage repayments and have more cash available to repay other loans. Secondly, interest only loans also give investors more control over their cash flow, by allowing them to keep their costs down and claim tax against their investment property.

Currently, interest-only mortgage loans are only available for up to a five-year fixed term. Whereas, in the last few years, the fixed term that borrowers could apply for an interest-only loan was up to 10 or 15 years.

Let’s look at an example of when an interest-only loan is due to end soon. You may have some investment properties with a combined remaining loan amount of $1.5 million. You are only paying interest on these loans now and the fixed term is ending soon. The default option is to move to a principal and interest loan, but you are worried that your current family net income is insufficient to cover the higher repayments. So, you might be wondering if you can get an extension on your interest-only mortgage.

So, the question is:

What should you do when your interest-only mortgage ends within two years?

Video Timeline

1. How does an interest-only loan vs a principal and interest loan affect your cash flow? - 00:07

2. What are your options when your interest-only mortgage is ending soon? - 03:00

1. How does an interest-only loan vs a principal and interest loan affect your cash flow?

Based on a 25-year loan of $1 million with a 4.3% interest-only mortgage rate, the required weekly payment is $865. In contrast, borrowers who have a principal and interest loan for the same loan amount would have to pay a total of $1,256 weekly. This equates to a difference of $391 between the two repayment options.

When your interest-only term is about to end, your lender will automatically switch you to a principal and interest loan. From the above interest-only loan example, we know the loan repayment will rise. It could be risky for you if you have insufficient cash flow to pay the mortgage.

Faced with the risk of insufficient cash flow when the interest-only term on your mortgage ends, you might consider increasing your rental fee on your investment properties. However, it seems unlikely that you can get an additional $400 (rounded-up) from your tenants. You also have the option to increase your job income to get more cash flow. But, on the whole, it’s not easy to get an additional $400 cash flow from an increase in your rental or job income.

If you are wondering how to calculate your interest-only loan repayments, you can check our handy mortgage calculator. By simply typing in your loan amount, loan term and current fixed interest rate, you will know exactly how much more principal and interest you will pay after your interest-only period ends.

Here’s the link for our mortgage calculator: http://prosperityfinance.co.nz/calculators

2. What are your options when your interest-only mortgage is ending soon?

What happens when interest only loan expires?

Our customers often ask us what they can do when they reach the end of an interest-only mortgage term. There are usually several options they can choose from.

Option 1: Get an interest-only extension from your existing lender

You can ask your current lender if it’s possible to extend your interest-only mortgage term to give you more time to pay it off.

Your lenders might need to check your current personal income and family situation, so that they can evaluate your ability to repay the mortgage over a longer period. Also, New Zealand bank policies are becoming a lot more conservative, which means there is no guarantee that you will get your interest-only loan extension approved by your current lender. Therefore, if you can’t prove that you have adequate income to cover the repayments, you might struggle to convince your lender to extend your term.

Option 2: Refinance your mortgage to another interest-only loan

If your current lender doesn’t extend the term of your interest-only loan, another option is to refinance to an interest-only loan with a different lender. You can continue to make interest-only repayments for another five years and keep your costs on your investment property down.

It all comes down to policy at a particular bank. Failing to get an interest-only loan extension approved from your current lender doesn’t necessarily mean that you can’t get approval from another bank.

Prosperity Finance enjoys a good relationship with many New Zealand lenders, which allows us to search through many home loan options and find the right lenders to suit your personal situation and needs.

When we review your loan and help you refinance your mortgage, Prosperity Finance can also help you secure other benefits, including improving your loan structure to protect your asset, reducing your loan interest and helping you pay off your loan faster.

Option 3: Start paying the principal and interest (P&I) with your current lender

What happens if neither an interest-only extension from your existing lender nor refinancing your mortgage to another interest-only loan suits you? In this case, your current lender will automatically switch you to a principal and interest loan when your interest-only loan term ends. This option might not be a bad idea – as you can start repaying the loan principal and interest if you have adequate cash flow to cover the repayments.

Option 4: Review your property portfolio

If the above three options are not available to you, you might need to consider other strategies when your interest-only mortgage expires, or is due to expire within the next two years.

Selling or downsizing your investment properties could help you reduce your loan repayments if you can’t afford it. You might make some money from the property sale and prevent ruining your credit score if your house prices have increased.

Disclaimer: The content in this article are provided for general situation purpose only. To the extent that any such information, opinions, views and recommendations constitute advice, they do not take into account any person’s particular financial situation or goals and, accordingly, do not constitute personalised financial advice. We therefore recommend that you seek advice from your adviser before taking any action.

Prosperity Finance - Here to help

Prosperity Finance looks at property investment strategically, empowering you to make the best long-term, informed decisions. We are professional mortgage brokers and are here to help. If your interest-only mortgage ends within the next two years, give us a call on 09 930 8999.

Other Blogs You Might Like:

Should I still refinance my mortgage even if my current rates are good?

Why should you consider refinancing your mortgage?

Archive

- April 2026 (1)

- February 2026 (1)

- December 2025 (1)

- October 2025 (1)

- August 2025 (2)

- July 2025 (1)

- June 2025 (2)

- April 2025 (1)

- October 2024 (1)

- July 2024 (1)

- June 2024 (1)

- April 2024 (1)

- January 2024 (1)

- December 2023 (1)

- November 2023 (3)

- October 2023 (3)

- September 2023 (3)

- August 2023 (2)

- July 2023 (4)

- June 2023 (2)

- May 2023 (5)

- April 2023 (4)

- March 2023 (2)

- February 2023 (3)

- November 2022 (4)

- October 2022 (1)

- September 2022 (2)

- August 2022 (1)

- July 2022 (4)

- June 2022 (2)

- April 2022 (1)

- March 2022 (3)

- February 2022 (1)

- December 2021 (3)

- November 2021 (3)

- October 2021 (3)

- September 2021 (3)

- August 2021 (2)

- July 2021 (2)

- June 2021 (2)

- May 2021 (3)

- April 2021 (3)

- March 2021 (3)

- February 2021 (4)

- January 2021 (3)

- December 2020 (3)

- November 2020 (4)

- October 2020 (3)

- September 2020 (2)

- August 2020 (2)

- July 2020 (5)

- June 2020 (3)

- May 2020 (3)

- April 2020 (4)

- March 2020 (4)

- February 2020 (3)

- January 2020 (3)

- December 2019 (1)

- November 2019 (4)

- October 2019 (5)

- September 2019 (4)

- August 2019 (4)

- July 2019 (5)

- June 2019 (4)

- May 2019 (5)

- April 2019 (3)

- March 2019 (5)

- February 2019 (3)

- January 2019 (1)

- November 2018 (1)

- October 2018 (1)

- January 2018 (4)