ANZ tightens servicing for rental property income, will this affect you?

Posted by: Connie in Property Investing

On 10 May, ANZ, one of New Zealand's biggest banks, has announced they would decrease the percentage of rental income they take into consideration when assessing new home loan application from 75 per cent to 65 per cent effective from 13 May, making the first move since the Government's announcement of new housing rules in 2021.

We're not surprised to see ANZ tighten their affordability criteria, and this is expected to happen. Back two weeks ago, we shared our view on how banks may change their lending policies to cope with New Zealand's housing reforms regarding the removal of interest deductions on the residential investment property. Investors will therefore have to pay more tax and have less cash in hand to service their loans.

In this video, we'll help you go through ANZ's announcement on rental income changes, use an example to quantify how your borrowing power may be reduced under ANZ's new rules, and analyse who will be impacted by the new rules, so that you can realize the urgency of applying for a home loan before it's too late.

ANZ tightens servicing for rental property income from 75% to 65%

Video Timeline

1. ANZ's rental income changes - 00:51

2. How will ANZ's policy change for rental property income affect your borrowing power? - 03:24

3. Will other banks follow suit and impose new serviceability rules? - 04:24

4. Who will be affected by ANZ's new calculation rules on affordability assessment? - 05:27

1. ANZ's rental income changes

ANZ's changes in rental property income are directly related to New Zealand's tax-deductibility changes. Under the recent rules, the interest costs on the residential investment property (non-new build) acquired on or after 27 March 2021 will no longer be able to offset against rental income.

Following the recent housing policy reforms, ANZ announced they would change how they treat rental income generating from residential investment properties.

In case you're not familiar with how banks calculate your rental property income: Instead of requiring a copy of financial statements for your rental property, banks calculate your rental income by a simple rule – only count a certain percentage (usually between 75 to 80% of your gross rental). They won't use 100% of your rental income because there are some costs involved in maintaining an investment property, such as insurance, rates, maintenance, and property management fee. Plus, banks also take the vacancy rate into consideration.

After they finish reviewing their current affordability assessment, they decided to change rental property income for new home loan applications in the following ways:

(1) Old calculation rules still apply to the residential property purchased before 27 March 2021 or derived from a new build or turnkey - 75% of the gross rental income may be used.

In our view, this is better than expected because for the property acquired before 27 March, the tax deductibility rule would be phased out over the next four years, which means your cashflow will be reduced gradually anyway, but ANZ hasn't reflected this difference to their new calculation.

(2) New calculation rules start applying to the residential property purchased on or after 27 March - 65% of the gross rental income may be used.

The new rules will come into effect on 13 May. The cutting off date is based on the application submission time. In other words, if you submit on or after 13 May, then the new rule will apply.

2. How will ANZ's policy change for rental property income affect your borrowing power?

ANZ's decision to only count 65% of rental income, down from 75%. This will undoubtedly decrease your borrowing capacity because ANZ takes less amount of rent into consideration when calculating the servicing.

To help you work out how the revised calculation used for affordability assessment can affect your borrowing power in practice, we're going to quantify the impact. Let's dive in:

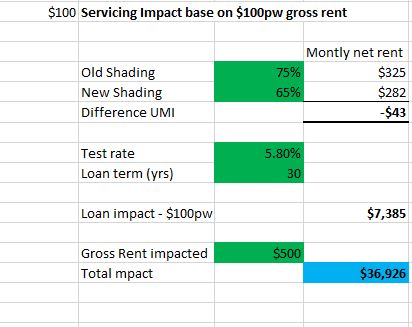

Say you're looking to buy an investment property that isn't a new build, and if you borrow the money from ANZ, for every $100 of weekly gross rental income:

After 65% of shading, your net rental income will be $282 per month, $43 less than it would be under the old rule. According to ANZ's current test rate (5.8%) and default loan repayment term (30 years), we can conclude for every $100 of weekly gross rent, the borrowing capacity will be reduced by $7,385.

If the rental income from the impacted investment property is $500 per week, which means the actual borrowing capacity will be reduced by $36,926 ($7,385 x 5) under ANZ's new servicing calculation.

3. Will other banks follow suit and impose new serviceability rules?

While ANZ is the first bank to tighten its affordability criteria for investors, and we wouldn't be surprised to see the other banks follow.

ANZ's new rule effectively reflects that property investors will have worse borrowing capacity under the recent housing reforms. Other banks are still in the process of review their lending policies as they know investors brace for cashflow hit due to the removal of the ability to offset their interest costs against their rental income. The changes are rolling in on the wheels of inevitability, and it is just a matter of time.

Note, if other banks impose their new assessment rules, the potentially reduced borrowing powers for investors can be different from under ANZ's new rule because there are three differentiating factors involved:

- Test rates – ANZ use 5.8% while other banks use different rates.

- Loan term – Not every bank allows for 30 years to repay an investment property loan. For example, ASB only allows for 25 years.

- Changes on shading percentage – ANZ announced to count 65% of rental income, down from 75%, while other banks may revise their servicing calculation differently.

4. Who will be affected by ANZ's new calculation rules on affordability assessment?

(1). Looking to borrow from ANZ? Its new affordability assessment will affect you if:

- Your existing investment properties are acquired on or after 27 March 2021, and they are not new builds. If so, even the purpose of your new loan is not for investment, you'll still be affected.

- You're applying for a home loan to purchase a property for investment purpose. Again, the property isn't a new build.

Note, the intergroup transaction is also defined as a purchase transaction. For example, in the scenario of upgrading home, your accountant may recommend you ‘sale’ your current home into a new entity with intention of long term hold investment property. If the date on the Sale and Purchase Agreement is on or after 27 March, then it's also affected by this new rule.

(2). Who won't be affected by ANZ's new rules?

- At the time of writing (12 May), ANZ is the first and the only bank that has made the decision to change the rental property income calculation rules. This means you still have a chance to apply for a home loan from other banks before they decrease the amount of rental income that is taken into consideration.

- You're buying a new build. New builds are exempt from ANZ's servicing calculator changes.

- You're looking to borrow money, and the borrowing purpose is not for purchasing an investment property, and your existing properties are acquired before 27 March, then you can apply from ANZ, and you'll still be assessed under their old rules.

Your action

ANZ decided to make the first significant change from the big four since the government' recent housing reforms, while other banks are very likely to follow suit. If you're thinking about applying for a home loan, act now while you may still be able to borrow more than later.

Again, we'll keep you updated with the latest lending policy changes and share our view on how the new rules may affect you.

Prosperity Finance - Here to Help

Want to know more about how the changes affect you? Or looking to apply for a home loan? Call us at 09 930 8999 to have a no-obligation chat with one of the financial advisors at Prosperity Finance to discuss your situation further.

Read more:

How may the removal of interest deductions hurt your borrowing power?

Restructure your loan before it’s too late

New housing policy 2021: Can investors still afford to hold the properties they have?

Disclaimer: The content in this article are provided for general situation purpose only. To the extent that any such information, opinions, views and recommendations constitute advice, they do not take into account any person’s particular financial situation or goals and, accordingly, do not constitute personalised financial advice. We therefore recommend that you seek advice from your adviser before taking any action.

On 10 May, ANZ, one of New Zealand's biggest banks, has announced they would decrease the percentage of rental income they take into consideration when assessing new home loan application from 75 per cent to 65 per cent effective from 13 May, making the first move since the Government's announcement of new housing rules in 2021.

We're not surprised to see ANZ tighten their affordability criteria, and this is expected to happen. Back two weeks ago, we shared our view on how banks may change their lending policies to cope with New Zealand's housing reforms regarding the removal of interest deductions on the residential investment property. Investors will therefore have to pay more tax and have less cash in hand to service their loans.

In this video, we'll help you go through ANZ's announcement on rental income changes, use an example to quantify how your borrowing power may be reduced under ANZ's new rules, and analyse who will be impacted by the new rules, so that you can realize the urgency of applying for a home loan before it's too late.

ANZ tightens servicing for rental property income from 75% to 65%

Video Timeline

1. ANZ's rental income changes - 00:51

2. How will ANZ's policy change for rental property income affect your borrowing power? - 03:24

3. Will other banks follow suit and impose new serviceability rules? - 04:24

4. Who will be affected by ANZ's new calculation rules on affordability assessment? - 05:27

1. ANZ's rental income changes

ANZ's changes in rental property income are directly related to New Zealand's tax-deductibility changes. Under the recent rules, the interest costs on the residential investment property (non-new build) acquired on or after 27 March 2021 will no longer be able to offset against rental income.

Following the recent housing policy reforms, ANZ announced they would change how they treat rental income generating from residential investment properties.

In case you're not familiar with how banks calculate your rental property income: Instead of requiring a copy of financial statements for your rental property, banks calculate your rental income by a simple rule – only count a certain percentage (usually between 75 to 80% of your gross rental). They won't use 100% of your rental income because there are some costs involved in maintaining an investment property, such as insurance, rates, maintenance, and property management fee. Plus, banks also take the vacancy rate into consideration.

After they finish reviewing their current affordability assessment, they decided to change rental property income for new home loan applications in the following ways:

(1) Old calculation rules still apply to the residential property purchased before 27 March 2021 or derived from a new build or turnkey - 75% of the gross rental income may be used.

In our view, this is better than expected because for the property acquired before 27 March, the tax deductibility rule would be phased out over the next four years, which means your cashflow will be reduced gradually anyway, but ANZ hasn't reflected this difference to their new calculation.

(2) New calculation rules start applying to the residential property purchased on or after 27 March - 65% of the gross rental income may be used.

The new rules will come into effect on 13 May. The cutting off date is based on the application submission time. In other words, if you submit on or after 13 May, then the new rule will apply.

2. How will ANZ's policy change for rental property income affect your borrowing power?

ANZ's decision to only count 65% of rental income, down from 75%. This will undoubtedly decrease your borrowing capacity because ANZ takes less amount of rent into consideration when calculating the servicing.

To help you work out how the revised calculation used for affordability assessment can affect your borrowing power in practice, we're going to quantify the impact. Let's dive in:

Say you're looking to buy an investment property that isn't a new build, and if you borrow the money from ANZ, for every $100 of weekly gross rental income:

After 65% of shading, your net rental income will be $282 per month, $43 less than it would be under the old rule. According to ANZ's current test rate (5.8%) and default loan repayment term (30 years), we can conclude for every $100 of weekly gross rent, the borrowing capacity will be reduced by $7,385.

If the rental income from the impacted investment property is $500 per week, which means the actual borrowing capacity will be reduced by $36,926 ($7,385 x 5) under ANZ's new servicing calculation.

3. Will other banks follow suit and impose new serviceability rules?

While ANZ is the first bank to tighten its affordability criteria for investors, and we wouldn't be surprised to see the other banks follow.

ANZ's new rule effectively reflects that property investors will have worse borrowing capacity under the recent housing reforms. Other banks are still in the process of review their lending policies as they know investors brace for cashflow hit due to the removal of the ability to offset their interest costs against their rental income. The changes are rolling in on the wheels of inevitability, and it is just a matter of time.

Note, if other banks impose their new assessment rules, the potentially reduced borrowing powers for investors can be different from under ANZ's new rule because there are three differentiating factors involved:

- Test rates – ANZ use 5.8% while other banks use different rates.

- Loan term – Not every bank allows for 30 years to repay an investment property loan. For example, ASB only allows for 25 years.

- Changes on shading percentage – ANZ announced to count 65% of rental income, down from 75%, while other banks may revise their servicing calculation differently.

4. Who will be affected by ANZ's new calculation rules on affordability assessment?

(1). Looking to borrow from ANZ? Its new affordability assessment will affect you if:

- Your existing investment properties are acquired on or after 27 March 2021, and they are not new builds. If so, even the purpose of your new loan is not for investment, you'll still be affected.

- You're applying for a home loan to purchase a property for investment purpose. Again, the property isn't a new build.

Note, the intergroup transaction is also defined as a purchase transaction. For example, in the scenario of upgrading home, your accountant may recommend you ‘sale’ your current home into a new entity with intention of long term hold investment property. If the date on the Sale and Purchase Agreement is on or after 27 March, then it's also affected by this new rule.

(2). Who won't be affected by ANZ's new rules?

- At the time of writing (12 May), ANZ is the first and the only bank that has made the decision to change the rental property income calculation rules. This means you still have a chance to apply for a home loan from other banks before they decrease the amount of rental income that is taken into consideration.

- You're buying a new build. New builds are exempt from ANZ's servicing calculator changes.

- You're looking to borrow money, and the borrowing purpose is not for purchasing an investment property, and your existing properties are acquired before 27 March, then you can apply from ANZ, and you'll still be assessed under their old rules.

Your action

ANZ decided to make the first significant change from the big four since the government' recent housing reforms, while other banks are very likely to follow suit. If you're thinking about applying for a home loan, act now while you may still be able to borrow more than later.

Again, we'll keep you updated with the latest lending policy changes and share our view on how the new rules may affect you.

Prosperity Finance - Here to Help

Want to know more about how the changes affect you? Or looking to apply for a home loan? Call us at 09 930 8999 to have a no-obligation chat with one of the financial advisors at Prosperity Finance to discuss your situation further.

Read more:

How may the removal of interest deductions hurt your borrowing power?

Restructure your loan before it’s too late

New housing policy 2021: Can investors still afford to hold the properties they have?

Disclaimer: The content in this article are provided for general situation purpose only. To the extent that any such information, opinions, views and recommendations constitute advice, they do not take into account any person’s particular financial situation or goals and, accordingly, do not constitute personalised financial advice. We therefore recommend that you seek advice from your adviser before taking any action.

Archive

- April 2026 (1)

- February 2026 (1)

- December 2025 (1)

- October 2025 (1)

- August 2025 (2)

- July 2025 (1)

- June 2025 (2)

- April 2025 (1)

- October 2024 (1)

- July 2024 (1)

- June 2024 (1)

- April 2024 (1)

- January 2024 (1)

- December 2023 (1)

- November 2023 (3)

- October 2023 (3)

- September 2023 (3)

- August 2023 (2)

- July 2023 (4)

- June 2023 (2)

- May 2023 (5)

- April 2023 (4)

- March 2023 (2)

- February 2023 (3)

- November 2022 (4)

- October 2022 (1)

- September 2022 (2)

- August 2022 (1)

- July 2022 (4)

- June 2022 (2)

- April 2022 (1)

- March 2022 (3)

- February 2022 (1)

- December 2021 (3)

- November 2021 (3)

- October 2021 (3)

- September 2021 (3)

- August 2021 (2)

- July 2021 (2)

- June 2021 (2)

- May 2021 (3)

- April 2021 (3)

- March 2021 (3)

- February 2021 (4)

- January 2021 (3)

- December 2020 (3)

- November 2020 (4)

- October 2020 (3)

- September 2020 (2)

- August 2020 (2)

- July 2020 (5)

- June 2020 (3)

- May 2020 (3)

- April 2020 (4)

- March 2020 (4)

- February 2020 (3)

- January 2020 (3)

- December 2019 (1)

- November 2019 (4)

- October 2019 (5)

- September 2019 (4)

- August 2019 (4)

- July 2019 (5)

- June 2019 (4)

- May 2019 (5)

- April 2019 (3)

- March 2019 (5)

- February 2019 (3)

- January 2019 (1)

- November 2018 (1)

- October 2018 (1)

- January 2018 (4)