Incorrectly converting home to investment property could cost you extra $7k a year

Posted by: Connie in Property Investing

When people upgrade their family home and keep their old home as an investment property, they can generally borrow the majority of the purchase cost if they have sufficient equity in their existing property portfolio. However, the interest on the new loan is not tax deductible against rental income from the old home as it fails the purpose of the loan test (i.e. the loan is for purchasing a new home, not for an investment property). As a result, the new investment property (i.e. the old home) generates big taxable profits.

In this week’s blog, we use a case study to discuss how a right loan structure could help you save ten thousands of dollars in tax each year when upgrading home.

Incorrectly converting home to investment property might cost you extra $7k a year

Video Timeline

1. When Luke and Jane upgrade home and keep their old home as an investment property, they could lose $7,789. -- 00:57

2. How could Luke and Jane save $7,789 annually by using right structure? -- 02:25

1. When Luke and Jane upgrade home and keep their old home as an investment property, they could lose $7,789

Luke and Jane, a married couple, plan to upgrade their family home. They can borrow the entire purchase costs of $930,000 for their new home as they have enough equity.

When the clients approached us, we analysed their situation and found that:

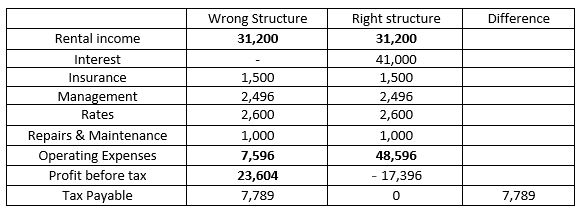

If they simply borrow $930,000 for the purchase of their new home, the interest on the $930,000 new debt won’t be tax deductible. Their old home is debt free with market value of $820,000 and rent appraisal of $600 per week (equivalent to $31,200 per year). Once they rent it out they expect to receive a rental income of $31,200 per year with their total operating expenses (insurance, rates, property management cost etc.) at $7,596 per year, producing a taxable profit of $23,604. At the 33% tax rate, they would have to pay $7,789 in tax.

2. How could Luke and Jane save $7,789 annually by using right structure?

If they first ‘sell’ their old home to a separate entity (company or trust), then that entity would be able to borrow 100% of the purchase price. As the purchase of the loan is to purchase an investment property, all of the interest costs on that loan are therefore tax deductible against the rental income – heavily reducing their taxable profit. In some situations where the investment property loan is large, your “look-through company” (LTC) is likely to incur a tax loss therefore they may qualify for tax refund.

The difference between these structures is tens of thousands of dollars in tax payments.

Had they moved the old home to a new structure and borrowed the money therein, the debt would have been tax deductible:

- The rent income is the same - $31,200 per year.

- Total operating expenses are the same - $7,596 per year.

- However under this structure, $41,000 of interest cost (on the $820,000 loan at 5% interest rate) is deductible, bringing the total deductions to $48,596 ($7,596 + $41,000).

- They incur a taxable loss of $17,396 ($31,200 - $48,596). With the correct structure, Luke and Jane could save $7,789.

So, if you’re thinking about upgrading family home, we highly recommend you ‘sell’ your old home to a separate entity, then that entity would be able to borrow 100% of the purchase price. All of the interest costs on that loan are therefore tax deductible against the rental income. Above all, talk to your professional tax accountant to make a personalized plan.

Prosperity Finance - here to help

Prosperity Finance looks at property investment strategically, empowering you to make the best long-term, informed decisions. We are professional mortgage brokers and are here to help. Give us a call today on 09 930 8999.

Other Recommended Blogs:

Turning your home into a rental property? Get the structure right

Your sale proceeds could be at risk when you hold multiple properties secured with one lender

Things to watch when turning your family home into an investment property

Disclaimer: The content in this article are provided for general situation purpose only. To the extent that any such information, opinions, views and recommendations constitute advice, they do not take into account any person’s particular financial situation or goals and, accordingly, do not constitute personalised financial advice. We therefore recommend that you seek advice from your adviser before taking any action.

When people upgrade their family home and keep their old home as an investment property, they can generally borrow the majority of the purchase cost if they have sufficient equity in their existing property portfolio. However, the interest on the new loan is not tax deductible against rental income from the old home as it fails the purpose of the loan test (i.e. the loan is for purchasing a new home, not for an investment property). As a result, the new investment property (i.e. the old home) generates big taxable profits.

In this week’s blog, we use a case study to discuss how a right loan structure could help you save ten thousands of dollars in tax each year when upgrading home.

Incorrectly converting home to investment property might cost you extra $7k a year

Video Timeline

1. When Luke and Jane upgrade home and keep their old home as an investment property, they could lose $7,789. -- 00:57

2. How could Luke and Jane save $7,789 annually by using right structure? -- 02:25

1. When Luke and Jane upgrade home and keep their old home as an investment property, they could lose $7,789

Luke and Jane, a married couple, plan to upgrade their family home. They can borrow the entire purchase costs of $930,000 for their new home as they have enough equity.

When the clients approached us, we analysed their situation and found that:

If they simply borrow $930,000 for the purchase of their new home, the interest on the $930,000 new debt won’t be tax deductible. Their old home is debt free with market value of $820,000 and rent appraisal of $600 per week (equivalent to $31,200 per year). Once they rent it out they expect to receive a rental income of $31,200 per year with their total operating expenses (insurance, rates, property management cost etc.) at $7,596 per year, producing a taxable profit of $23,604. At the 33% tax rate, they would have to pay $7,789 in tax.

2. How could Luke and Jane save $7,789 annually by using right structure?

If they first ‘sell’ their old home to a separate entity (company or trust), then that entity would be able to borrow 100% of the purchase price. As the purchase of the loan is to purchase an investment property, all of the interest costs on that loan are therefore tax deductible against the rental income – heavily reducing their taxable profit. In some situations where the investment property loan is large, your “look-through company” (LTC) is likely to incur a tax loss therefore they may qualify for tax refund.

The difference between these structures is tens of thousands of dollars in tax payments.

Had they moved the old home to a new structure and borrowed the money therein, the debt would have been tax deductible:

- The rent income is the same - $31,200 per year.

- Total operating expenses are the same - $7,596 per year.

- However under this structure, $41,000 of interest cost (on the $820,000 loan at 5% interest rate) is deductible, bringing the total deductions to $48,596 ($7,596 + $41,000).

- They incur a taxable loss of $17,396 ($31,200 - $48,596). With the correct structure, Luke and Jane could save $7,789.

So, if you’re thinking about upgrading family home, we highly recommend you ‘sell’ your old home to a separate entity, then that entity would be able to borrow 100% of the purchase price. All of the interest costs on that loan are therefore tax deductible against the rental income. Above all, talk to your professional tax accountant to make a personalized plan.

Prosperity Finance - here to help

Prosperity Finance looks at property investment strategically, empowering you to make the best long-term, informed decisions. We are professional mortgage brokers and are here to help. Give us a call today on 09 930 8999.

Other Recommended Blogs:

Turning your home into a rental property? Get the structure right

Your sale proceeds could be at risk when you hold multiple properties secured with one lender

Things to watch when turning your family home into an investment property

Disclaimer: The content in this article are provided for general situation purpose only. To the extent that any such information, opinions, views and recommendations constitute advice, they do not take into account any person’s particular financial situation or goals and, accordingly, do not constitute personalised financial advice. We therefore recommend that you seek advice from your adviser before taking any action.

Archive

- April 2026 (1)

- February 2026 (1)

- December 2025 (1)

- October 2025 (1)

- August 2025 (2)

- July 2025 (1)

- June 2025 (2)

- April 2025 (1)

- October 2024 (1)

- July 2024 (1)

- June 2024 (1)

- April 2024 (1)

- January 2024 (1)

- December 2023 (1)

- November 2023 (3)

- October 2023 (3)

- September 2023 (3)

- August 2023 (2)

- July 2023 (4)

- June 2023 (2)

- May 2023 (5)

- April 2023 (4)

- March 2023 (2)

- February 2023 (3)

- November 2022 (4)

- October 2022 (1)

- September 2022 (2)

- August 2022 (1)

- July 2022 (4)

- June 2022 (2)

- April 2022 (1)

- March 2022 (3)

- February 2022 (1)

- December 2021 (3)

- November 2021 (3)

- October 2021 (3)

- September 2021 (3)

- August 2021 (2)

- July 2021 (2)

- June 2021 (2)

- May 2021 (3)

- April 2021 (3)

- March 2021 (3)

- February 2021 (4)

- January 2021 (3)

- December 2020 (3)

- November 2020 (4)

- October 2020 (3)

- September 2020 (2)

- August 2020 (2)

- July 2020 (5)

- June 2020 (3)

- May 2020 (3)

- April 2020 (4)

- March 2020 (4)

- February 2020 (3)

- January 2020 (3)

- December 2019 (1)

- November 2019 (4)

- October 2019 (5)

- September 2019 (4)

- August 2019 (4)

- July 2019 (5)

- June 2019 (4)

- May 2019 (5)

- April 2019 (3)

- March 2019 (5)

- February 2019 (3)

- January 2019 (1)

- November 2018 (1)

- October 2018 (1)

- January 2018 (4)