Is it better to buy an investment property before first home?

Posted by: Connie in Property Investing

Purchasing a home to live in feels like a rite of passage for many people. If you’re in the market to buy your first home, have you ever wondered is it better to buy an investment property first or buy a home to live in first?

In this article, we’ll discuss 4 reasons why some people consider buying an investment property before first home, especially with current trends in New Zealand real estate market. We’ll also learn about the difference between buying a rental property and buying an owner-occupied property that every first-time buyer needs to know about, such as the deposit requirement, how banks calculate your servicing for home loan, etc.

As mortgage brokers, when we asked our clients the intention of purchase, we often had answers of maybe home or maybe an investment property. It’s okay to be open-minded at the enquiry stage but we suggest that you should make a decision before loan application as there are many different aspects between the two. When we make application to the bank, we can only have one purpose (one way or another, can’t be both). If your intention is for a primary residence, for example, but you rent it out, then there could be some tax implications.

Is it better to buy an investment property before first home?

Video Timeline

1. Why buying an investment property before your first home? - 01:25

2. The difference between buying an investment property and a first home to live in - 03:33

1. Why buying an investment property before your first home?

Here are the main reasons for some first-time property buyers buying a rental property before primary residence:

(1) You’re living with your parents

If you’re living together with your parents, you only pay a little or no rents at all, and you have the ability to borrow, then buying an investment property can be a great choice. It helps you get onto the property ladder early and build wealth fast.

(2) You have limited budget

Given the current trends of real estate market in New Zealand, especially in Auckland, the ideal first home probably worth one million dollars. If you only have limited budget on buying a property due to your borrowing capacity and the deposit you have, you may only afford $800K, for example. In this case, you might want to buy an investment property first, rather than waiting for several years.

(3) The location isn’t ideal for home

Let’s say you have your eye on a property that can be a great investment, but the location of the property is far away from your office or your kid’s school, or even not in the city where you’re currently living. Instead of missing out this opportunity, you decided to purchase this as a rental property.

(4) You’re planning for your future move

For example, if you currently live in Auckland, and you’re planning to relocate to another location. Maybe because you love the lifestyle there, or perhaps you want to live closer to your family in the future. So you can secure that property right now and rent it out.

2. The difference between buying an investment property and a first home to live in

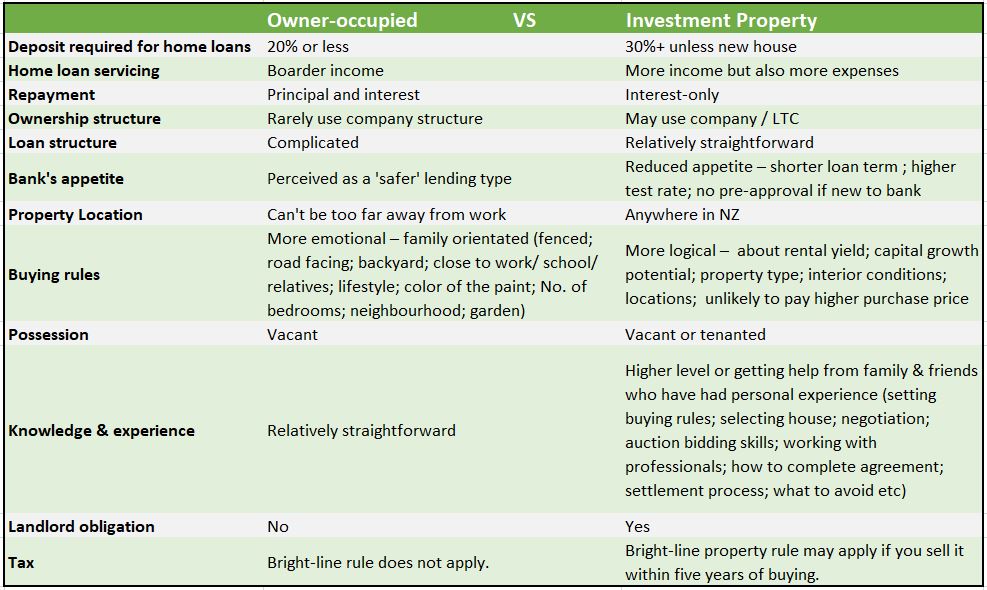

(1) Deposit required for home loans

If you want to buy your first home as an owner-occupied, you’re required to have 5% - 20% deposit. Whereas you need to have at least 30% deposit when borrowing for an investment property, some banks require 40% now, unless you’re buying a new property which is exempt from LVR rule.

(2) Home loan servicing

When New Zealand banks calculate how much you can borrow, they’ll consider your deposit and your income. Your income determines how much home loan you can afford to borrow, also known as servicing ability.

If you’re borrowing for your primary residence, you can have boarders. In other words, your bank will factor in your boarder income. But if you’re borrowing for your rental property as your first property, banks will consider not only your rental income, but also your rent expense unless you live with your family for free. So, the net income can be quite different, and it affects your servicing ability.

(3) Home loan repayment

For owner-occupied, it's common to see principal and interest repayments. Interest-only isn’t impossible, but it happens rare because banks may wonder are you expecting financial hardship or something like that? On the contrary, interest-only is a common repayment method, especially if you still have loan for your family home, it not only helps you pay off home loan faster but also more tax efficient.

(4) Ownership structure

With owner-occupied property, company structure is very rare unless you had it as an investment property at the beginning and then later you move into that property and didn’t want to change the ownership. Otherwise, it is normally under a personal name or family trust. Whereas it’s common to have a company structure for a rental property.

(5) Loan structure

You’re planning to upgrade home, say you already have a home, and you want to keep your current home, we’d suggest seeking help from your mortgage broker and tax accountant to see if there is a better way to structure your loan so that it minimises your tax obligation rather than borrowing entirely for the new home purpose. In contrast, the finance structure for a rental property is relatively straightforward.

(6) Lending appetite

Banks perceive owner-occupied as a safer lending type because no one wants to lose their home while rental property is just an investment vehicle. To manage risks, banks have stricter lending policies for investment property loans.

For example, the loan term for an investment property is shorter; the test rates (interest rates are used by banks to assess new loan affordability) can be higher resulting in less borrowing; some banks don't do pre-approvals for new-to-bank customers to buy a rental property but they're happy with owner-occupied property.

(7) Location

When considering a place to live in, you often want to choose for convenience, such as close to your office. But when it comes to the location of a rental property, your personal preference doesn’t matter. Instead, you’ll choose the location based on investment strategy and it can be in any cities/areas in New Zealand, as long as it meets your criteria.

(8) Buying rules

Buying your home often involve emotional decisions – You may not want to purchase a property in a quiet street rather than road-front; you want to have a backyard for your kids to have a safe place to play; you prefer living close to work… Sometimes when you fall in love with a property, these emotional factors are very unique to you and you don’t mind paying premium price as long as it tickets the boxes.

When buying a rental property, you have your buying rules that are built with a logical mind. It often includes the rental yield, the capital growth potential, the property’s condition, the location, et cetera. When you stick to your buying rules, you normally won’t go over your budget unless it has huge potential.

(9) Possession

Possession means when you purchase a property if there are existing tenants or not. If you’re buying an owner-occupied property, you can't have tenants to the property because you want to live there while for a rental property, it can be vacant or tenanted. And normally you want it tenanted so that you can have rental income from day one.

(10) Your knowledge and experience about property and finance

Buying a house for owner-occupied purpose is relatively straightforward, especially when your situation is simple, and you have good advisors around you for legal matters and finance.

On the contrary, when buying an investment property, you’ll need a higher level of skills in setting buying rules, property selection, price negotiation, and agreement conditions. Plus, you need experience on auction and be familiar with the settlement process as well. Finance structure is also more sophisticated.

(11) Your legal obligations as a landlord

As a residential landlord, your obligations are covered by the Residential Tenancies Act and Regulations. You need to ensure that you are aware of these requirements. It’s becoming much more complicated and important than before. For example, you can ask your tenants to move out without giving a specific reason while this isn’t allowed now and you have to tell tenants 90 days in advance; If your rental property doesn’t meet the minimum standards for healthy homes, you’re at risk of facing a penalty.

(12) Bright Line Rule

If you buy a rental property and you sell it within five years, you may need to pay tax. Owner occupied properties on the other hand are exempt from the rules.

It is important for you to consider the intention of buying a property before you lodge the home loan application. If you do not follow your intention as you declare to the bank, it could have these differences and implications we’ve covered above.

Prosperity Finance - Here to Help

If you’re thinking about buying an investment property before first home, or buying a home to live in first, we’re here to help. Call us at 09 930 8999 for a chat with one of our mortgage advisors. We’ll look at your case, understand your needs and situation then make a tailored solution for you.

Read More:

ANZ now requires 40% deposit for residential property investment loan

Mortgage serviceability test rates have finally dropped – You may afford to borrow more now

Turning your home into a rental property? Get the structure right

Disclaimer: The content in this article are provided for general situation purpose only. To the extent that any such information, opinions, views and recommendations constitute advice, they do not take into account any person’s particular financial situation or goals and, accordingly, do not constitute personalised financial advice. We therefore recommend that you seek advice from your adviser before taking any action.

Purchasing a home to live in feels like a rite of passage for many people. If you’re in the market to buy your first home, have you ever wondered is it better to buy an investment property first or buy a home to live in first?

In this article, we’ll discuss 4 reasons why some people consider buying an investment property before first home, especially with current trends in New Zealand real estate market. We’ll also learn about the difference between buying a rental property and buying an owner-occupied property that every first-time buyer needs to know about, such as the deposit requirement, how banks calculate your servicing for home loan, etc.

As mortgage brokers, when we asked our clients the intention of purchase, we often had answers of maybe home or maybe an investment property. It’s okay to be open-minded at the enquiry stage but we suggest that you should make a decision before loan application as there are many different aspects between the two. When we make application to the bank, we can only have one purpose (one way or another, can’t be both). If your intention is for a primary residence, for example, but you rent it out, then there could be some tax implications.

Is it better to buy an investment property before first home?

Video Timeline

1. Why buying an investment property before your first home? - 01:25

2. The difference between buying an investment property and a first home to live in - 03:33

1. Why buying an investment property before your first home?

Here are the main reasons for some first-time property buyers buying a rental property before primary residence:

(1) You’re living with your parents

If you’re living together with your parents, you only pay a little or no rents at all, and you have the ability to borrow, then buying an investment property can be a great choice. It helps you get onto the property ladder early and build wealth fast.

(2) You have limited budget

Given the current trends of real estate market in New Zealand, especially in Auckland, the ideal first home probably worth one million dollars. If you only have limited budget on buying a property due to your borrowing capacity and the deposit you have, you may only afford $800K, for example. In this case, you might want to buy an investment property first, rather than waiting for several years.

(3) The location isn’t ideal for home

Let’s say you have your eye on a property that can be a great investment, but the location of the property is far away from your office or your kid’s school, or even not in the city where you’re currently living. Instead of missing out this opportunity, you decided to purchase this as a rental property.

(4) You’re planning for your future move

For example, if you currently live in Auckland, and you’re planning to relocate to another location. Maybe because you love the lifestyle there, or perhaps you want to live closer to your family in the future. So you can secure that property right now and rent it out.

2. The difference between buying an investment property and a first home to live in

(1) Deposit required for home loans

If you want to buy your first home as an owner-occupied, you’re required to have 5% - 20% deposit. Whereas you need to have at least 30% deposit when borrowing for an investment property, some banks require 40% now, unless you’re buying a new property which is exempt from LVR rule.

(2) Home loan servicing

When New Zealand banks calculate how much you can borrow, they’ll consider your deposit and your income. Your income determines how much home loan you can afford to borrow, also known as servicing ability.

If you’re borrowing for your primary residence, you can have boarders. In other words, your bank will factor in your boarder income. But if you’re borrowing for your rental property as your first property, banks will consider not only your rental income, but also your rent expense unless you live with your family for free. So, the net income can be quite different, and it affects your servicing ability.

(3) Home loan repayment

For owner-occupied, it's common to see principal and interest repayments. Interest-only isn’t impossible, but it happens rare because banks may wonder are you expecting financial hardship or something like that? On the contrary, interest-only is a common repayment method, especially if you still have loan for your family home, it not only helps you pay off home loan faster but also more tax efficient.

(4) Ownership structure

With owner-occupied property, company structure is very rare unless you had it as an investment property at the beginning and then later you move into that property and didn’t want to change the ownership. Otherwise, it is normally under a personal name or family trust. Whereas it’s common to have a company structure for a rental property.

(5) Loan structure

You’re planning to upgrade home, say you already have a home, and you want to keep your current home, we’d suggest seeking help from your mortgage broker and tax accountant to see if there is a better way to structure your loan so that it minimises your tax obligation rather than borrowing entirely for the new home purpose. In contrast, the finance structure for a rental property is relatively straightforward.

(6) Lending appetite

Banks perceive owner-occupied as a safer lending type because no one wants to lose their home while rental property is just an investment vehicle. To manage risks, banks have stricter lending policies for investment property loans.

For example, the loan term for an investment property is shorter; the test rates (interest rates are used by banks to assess new loan affordability) can be higher resulting in less borrowing; some banks don't do pre-approvals for new-to-bank customers to buy a rental property but they're happy with owner-occupied property.

(7) Location

When considering a place to live in, you often want to choose for convenience, such as close to your office. But when it comes to the location of a rental property, your personal preference doesn’t matter. Instead, you’ll choose the location based on investment strategy and it can be in any cities/areas in New Zealand, as long as it meets your criteria.

(8) Buying rules

Buying your home often involve emotional decisions – You may not want to purchase a property in a quiet street rather than road-front; you want to have a backyard for your kids to have a safe place to play; you prefer living close to work… Sometimes when you fall in love with a property, these emotional factors are very unique to you and you don’t mind paying premium price as long as it tickets the boxes.

When buying a rental property, you have your buying rules that are built with a logical mind. It often includes the rental yield, the capital growth potential, the property’s condition, the location, et cetera. When you stick to your buying rules, you normally won’t go over your budget unless it has huge potential.

(9) Possession

Possession means when you purchase a property if there are existing tenants or not. If you’re buying an owner-occupied property, you can't have tenants to the property because you want to live there while for a rental property, it can be vacant or tenanted. And normally you want it tenanted so that you can have rental income from day one.

(10) Your knowledge and experience about property and finance

Buying a house for owner-occupied purpose is relatively straightforward, especially when your situation is simple, and you have good advisors around you for legal matters and finance.

On the contrary, when buying an investment property, you’ll need a higher level of skills in setting buying rules, property selection, price negotiation, and agreement conditions. Plus, you need experience on auction and be familiar with the settlement process as well. Finance structure is also more sophisticated.

(11) Your legal obligations as a landlord

As a residential landlord, your obligations are covered by the Residential Tenancies Act and Regulations. You need to ensure that you are aware of these requirements. It’s becoming much more complicated and important than before. For example, you can ask your tenants to move out without giving a specific reason while this isn’t allowed now and you have to tell tenants 90 days in advance; If your rental property doesn’t meet the minimum standards for healthy homes, you’re at risk of facing a penalty.

(12) Bright Line Rule

If you buy a rental property and you sell it within five years, you may need to pay tax. Owner occupied properties on the other hand are exempt from the rules.

It is important for you to consider the intention of buying a property before you lodge the home loan application. If you do not follow your intention as you declare to the bank, it could have these differences and implications we’ve covered above.

Prosperity Finance - Here to Help

If you’re thinking about buying an investment property before first home, or buying a home to live in first, we’re here to help. Call us at 09 930 8999 for a chat with one of our mortgage advisors. We’ll look at your case, understand your needs and situation then make a tailored solution for you.

Read More:

ANZ now requires 40% deposit for residential property investment loan

Mortgage serviceability test rates have finally dropped – You may afford to borrow more now

Turning your home into a rental property? Get the structure right

Disclaimer: The content in this article are provided for general situation purpose only. To the extent that any such information, opinions, views and recommendations constitute advice, they do not take into account any person’s particular financial situation or goals and, accordingly, do not constitute personalised financial advice. We therefore recommend that you seek advice from your adviser before taking any action.

Archive

- April 2026 (1)

- February 2026 (1)

- December 2025 (1)

- October 2025 (1)

- August 2025 (2)

- July 2025 (1)

- June 2025 (2)

- April 2025 (1)

- October 2024 (1)

- July 2024 (1)

- June 2024 (1)

- April 2024 (1)

- January 2024 (1)

- December 2023 (1)

- November 2023 (3)

- October 2023 (3)

- September 2023 (3)

- August 2023 (2)

- July 2023 (4)

- June 2023 (2)

- May 2023 (5)

- April 2023 (4)

- March 2023 (2)

- February 2023 (3)

- November 2022 (4)

- October 2022 (1)

- September 2022 (2)

- August 2022 (1)

- July 2022 (4)

- June 2022 (2)

- April 2022 (1)

- March 2022 (3)

- February 2022 (1)

- December 2021 (3)

- November 2021 (3)

- October 2021 (3)

- September 2021 (3)

- August 2021 (2)

- July 2021 (2)

- June 2021 (2)

- May 2021 (3)

- April 2021 (3)

- March 2021 (3)

- February 2021 (4)

- January 2021 (3)

- December 2020 (3)

- November 2020 (4)

- October 2020 (3)

- September 2020 (2)

- August 2020 (2)

- July 2020 (5)

- June 2020 (3)

- May 2020 (3)

- April 2020 (4)

- March 2020 (4)

- February 2020 (3)

- January 2020 (3)

- December 2019 (1)

- November 2019 (4)

- October 2019 (5)

- September 2019 (4)

- August 2019 (4)

- July 2019 (5)

- June 2019 (4)

- May 2019 (5)

- April 2019 (3)

- March 2019 (5)

- February 2019 (3)

- January 2019 (1)

- November 2018 (1)

- October 2018 (1)

- January 2018 (4)