Mortgage serviceability test rates have finally dropped – You may afford to borrow more now

Posted by: Connie in Finance 101

When it comes to how much you can borrow for a mortgage, a lender will consider many factors when deciding whether to approve your application. There are two main factors that New Zealand lenders consider:

- Home loan deposit – cash, or equity from your current properties (Please refer to this article)

- Serviceability – how much loan you can afford base on your net income

In this article, we bring you with good news – two New Zealand banks have reduced the rates they use to test borrowers’ ability to service their loans. We explain how banks work out the serviceability and discuss how the reduced serviceability test rate can have a positive influence on your borrowing power, using a case study.

Mortgage serviceability test rates have finally dropped – You may afford to borrow more

Video Timeline

1. What is mortgage serviceability rate? - 01:22

2. How much more mortgage can you afford as the result of reduced serviceability test rates? - 02:41

3. Other factors affecting serviceability - how much mortgage you can afford - 08:32

4. Is it much harder to get a home loan now (post Covid-19)? - 10:18

5. How can I improve my home loan serviceability? - 12:08

6. The secret revealed: exposing the serviceability test rates that New Zealand banks are using to assess your home loan application (updating on July 2020) - 14:02

1. What is mortgage serviceability rate?

New Zealand banks use mortgage serviceability rate of 6% -7% to assess the borrowing power of borrowers to repay their home loan, regardless of the actual current interest rates are. The reason for them to use serviceability rate that much higher is because once they approve the home loan, they commit to you for 25- 30 years. New Zealand mortgage interest rates can fluctuate. Currently, the interest rate of 2.55% hits the historically low, but that does not mean it cannot go up in the future.

Two New Zealand banks have reduced their mortgage serviceability rate they use to assess borrowers’ ability to repay the loans:

- Bank of China (BOC) dropped their serviceability rate dramatically, from 6.25% to 5.0%

- ASB cut their serviceability rate from 7.2% to 6.45%

2. How much more mortgage can you afford as the result of reduced serviceability test rates?

In general, banks calculate your home loan serviceability by adding together all your net income, subtracting your living expenses and any financial commitment such as existing loan.

Here’s a case study to illustrate how New Zealand banks calculate how much mortgage you can afford to borrow based on your income, expenses and existing debt:

Say a couple, Tony and his wife, have two kids. Tony works as an IT expert, with a gross income of $115k annually. His wife is a housewife.

Currently, Tony and his wife rent for $700 a week. They are wondering if they can buy their first home around $1.3 million, then they can stop paying for someone else mortgage.

How could they benefit from a lower serviceability test rate?

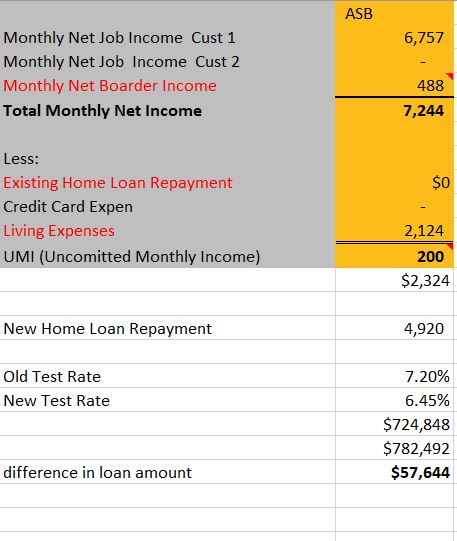

(1) How does ASB calculate their borrowing power? And how much more can they afford to borrow with a lower test rate?

From Income perspective

- Monthly job income – Tony’s net job income on a monthly basis, after Kiwisaver and PAYE, is $6,757

- Monthly net boarder income – they consider buying a five-bedroom house and they propose to have two boarders at their new home to help them ease the stress of mortgage payments. As ASB only consider taking one boarder and plus discount at 75%, their monthly net boarder income is $488

Total monthly net income = $6,757 + $488 = $7,244

From expenses perspective

- Existing home loan repayment – they are first home buyer, so they don't have any existing home loan

- Credit card – they do not have a credit card

- Living expenses – each lender has their own model to calculate your living expenses. The calculation is mainly based on the household income and family structure (how many adults, how many kids). Some lenders also believe the income does make a difference. The more income you earn, the more living expense you have. From the view of ASB, the amount of their minimum living expenses is $2124

- UMI (Uncommitted Monthly Income) – lenders work out what surplus a borrower has left after all of their current obligations are taken from their incomes. Lenders use what we call a UMI to measure this. ASB require $200

Total monthly expenses = $2124 + $200 = $2,324

After combing their expenses and incomes, the available amount that can be used to repay their new home loan is $4,920 (the monthly net income minus the net expenses)

Under previous serviceability test rate (7.2%), they can borrow $724K. But with the rate easing to 6.45%, they can borrow $782k from ASB. First home buyers like Tony and his wife are seeing their borrowing power increase by as much $;60k nearly.

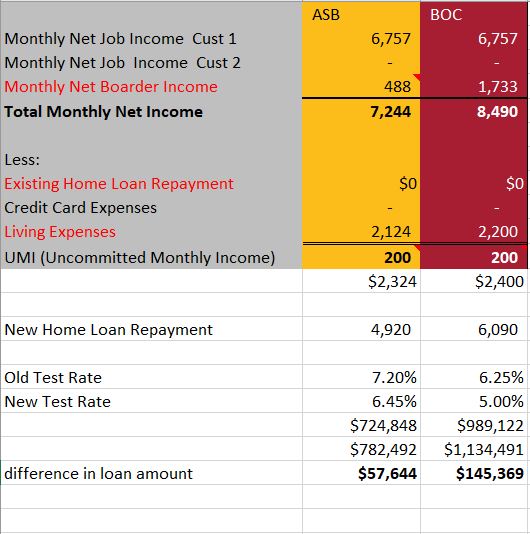

(2) How does Bank of China (BOC) calculate their borrowing power? And how much more can they afford to borrow with a lower test rate?

If you deal with different lenders, you will get different loan amounts. When Bank of China calculate how much Tony and his wife can afford to borrow, they apply the different calculating model. The difference mainly comes from:

- Monthly net boarder income – Bank of China are happy to take two boarder income, and they take 100% (not like ASB taking discount). That’s why Tony’s monthly boarder income is much higher ($1,733) from the view of BOC

- Living expenses – the calculation from Bank of China ($2,200) is just slightly higher than ASB

So, from the perspective of Bank of China, the amount that can be used to repay Tony’s new home loan ($1,170) is higher than ASB

What we want to point out is, compared with the borrowing power ($989k) under the previous serviceability test rate (6.25%), now they can afford to borrow as much high as $113k - $145k more than they could before.

It’s important to note that your borrowing power will vary between lenders. If you get an offer from one lender, it does not mean you'll get a similar amount from the other, and it could have a massive difference like in this case.

3. Other factors affecting serviceability - how much mortgage you can afford

From the above case, you have understood how the serviceability test rate can affect your home loan borrowing power in a huge way. Apart from the test rate, here are some other factors that have big impact when working out your serviceability:

(1) Existing home loan

Mortgage lenders will take all your existing home loan into account when deciding whether you are eligible for a mortgage and how much you can afford to borrow. They’ll look at details of your existing loan, such as the current mortgage rates you’re repaying, the loan maturity dates, the repayment method (principal and interest, or interest only). So, if you improve the structure on your existing home loan, then it can make a huge difference on your future borrowing capacity.

(2) Living expenses

Banks use different methods to calculate your living expenses. With that saying, the calculation for the same case may vary between different banks.

(3) Boarder income

Some banks only allow a maximum of $150 - $200 per week to be used to pay a mortgage. Even though in some cities, it is easy to get more than that as rent. But banks don’t want to assume the very best-case scenario, they want to cap the amount to see if you can afford a mortgage. However, some banks do not set a cap amount. Also, some banks only consider one boarder income, regardless of how many spare bedrooms you have, while other banks allow two boarders.

So, not all lenders have the same serviceability assessment and apply the same test rate. It’s all about choosing the lender that suits your needs and situation best, and improving your existing home loan structure, then you may dramatically improve your borrowing power.

4. Is it much harder to get a home loan now (post Covid-19)?

Thinking about applying for a new loan during the post Covid-19? Some people comment it is harder to get a mortgage since the Covid-19. Our view is:

Yes, after Covid-19, banks have tightened up their lending policy, specifically regarding your income.

- If you are self-employed and your business just recovered from Covid-19, then it is probably too early for the bank to get comfort around your outgoing income.

- If you have recently moved into a new job for less than three months, then some banks may not consider your job as stable income until six months.

- If currently you don’t receive any rental income, maybe your parents are living in your property, or maybe your tenants just leave, then banks may not happy to use a rental appraisal because Covid-19 has caused New Zealand rental property market to fluctuate. We’ve seen the rent has reduced in some parts of New Zealand.

However, if your income is stable and you can prove your incomes, then in our view your borrowing capacity is increasing now. You can afford to borrow more than you could before.

5. How can I improve my home loan serviceability?

If you are looking to borrow money to buy a property and you have enough deposit or equity in your existing property, then your serviceability determines how much you can borrow. The followings are some of our recommendations:

First, you need to engage with an experienced and responsible mortgage advisor as early as possible. Do not wait until you find your dream property and plan to buy within a few days, then it is too late.

At Prosperity Finance, we don’t have a one-size-fits-all solution for your home loan. We look at your individual case, understand your needs and situation then make a tailored solution for you. That’s why it takes much time for us to do the preparation work, including:

- Does your existing home loan structure work well for you?

- Have you moved the equity to the bank that can lend you the most, so that you can borrow more to buy your next property?

- When it comes to home loan re-fix or refinance, it's important to think about your plan so that we know how long you should fix for and whether or not you should consider refinancing, etc.

6. The secret revealed: exposing the serviceability test rates that New Zealand banks are using to assess your home loan application (updating on July 2020)

Do you want to know the test rate your bank use? Here we reveal some of them, then it gives you the indication of what levels of the rates they are using to assess your application.

ANZ 6.65%

ASB 6.45%

BNZ 6.75%

Westpac 7.25%

Bank of China 5.0%

and we expect that more banks are considering reducing their test rates soon.

Prosperity Finance – here to help

We can assess your situation for free and give you an indication of how much you can afford to borrow. Call us at 09 930 8999 for a no-obligation chat with our adviser.

Other Blogs You Might Like:

LVR restriction removed and what does it mean for you?

Top 5 reasons your home loan application is declined and what you need to avoid

Incorrectly converting home to investment property could cost you extra $7k a year

Disclaimer: The content in this article are provided for general situation purpose only. To the extent that any such information, opinions, views and recommendations constitute advice, they do not take into account any person’s particular financial situation or goals and, accordingly, do not constitute personalised financial advice. We therefore recommend that you seek advice from your adviser before taking any action.

When it comes to how much you can borrow for a mortgage, a lender will consider many factors when deciding whether to approve your application. There are two main factors that New Zealand lenders consider:

- Home loan deposit – cash, or equity from your current properties (Please refer to this article)

- Serviceability – how much loan you can afford base on your net income

In this article, we bring you with good news – two New Zealand banks have reduced the rates they use to test borrowers’ ability to service their loans. We explain how banks work out the serviceability and discuss how the reduced serviceability test rate can have a positive influence on your borrowing power, using a case study.

Mortgage serviceability test rates have finally dropped – You may afford to borrow more

Video Timeline

1. What is mortgage serviceability rate? - 01:22

2. How much more mortgage can you afford as the result of reduced serviceability test rates? - 02:41

3. Other factors affecting serviceability - how much mortgage you can afford - 08:32

4. Is it much harder to get a home loan now (post Covid-19)? - 10:18

5. How can I improve my home loan serviceability? - 12:08

6. The secret revealed: exposing the serviceability test rates that New Zealand banks are using to assess your home loan application (updating on July 2020) - 14:02

1. What is mortgage serviceability rate?

New Zealand banks use mortgage serviceability rate of 6% -7% to assess the borrowing power of borrowers to repay their home loan, regardless of the actual current interest rates are. The reason for them to use serviceability rate that much higher is because once they approve the home loan, they commit to you for 25- 30 years. New Zealand mortgage interest rates can fluctuate. Currently, the interest rate of 2.55% hits the historically low, but that does not mean it cannot go up in the future.

Two New Zealand banks have reduced their mortgage serviceability rate they use to assess borrowers’ ability to repay the loans:

- Bank of China (BOC) dropped their serviceability rate dramatically, from 6.25% to 5.0%

- ASB cut their serviceability rate from 7.2% to 6.45%

2. How much more mortgage can you afford as the result of reduced serviceability test rates?

In general, banks calculate your home loan serviceability by adding together all your net income, subtracting your living expenses and any financial commitment such as existing loan.

Here’s a case study to illustrate how New Zealand banks calculate how much mortgage you can afford to borrow based on your income, expenses and existing debt:

Say a couple, Tony and his wife, have two kids. Tony works as an IT expert, with a gross income of $115k annually. His wife is a housewife.

Currently, Tony and his wife rent for $700 a week. They are wondering if they can buy their first home around $1.3 million, then they can stop paying for someone else mortgage.

How could they benefit from a lower serviceability test rate?

(1) How does ASB calculate their borrowing power? And how much more can they afford to borrow with a lower test rate?

From Income perspective

- Monthly job income – Tony’s net job income on a monthly basis, after Kiwisaver and PAYE, is $6,757

- Monthly net boarder income – they consider buying a five-bedroom house and they propose to have two boarders at their new home to help them ease the stress of mortgage payments. As ASB only consider taking one boarder and plus discount at 75%, their monthly net boarder income is $488

Total monthly net income = $6,757 + $488 = $7,244

From expenses perspective

- Existing home loan repayment – they are first home buyer, so they don't have any existing home loan

- Credit card – they do not have a credit card

- Living expenses – each lender has their own model to calculate your living expenses. The calculation is mainly based on the household income and family structure (how many adults, how many kids). Some lenders also believe the income does make a difference. The more income you earn, the more living expense you have. From the view of ASB, the amount of their minimum living expenses is $2124

- UMI (Uncommitted Monthly Income) – lenders work out what surplus a borrower has left after all of their current obligations are taken from their incomes. Lenders use what we call a UMI to measure this. ASB require $200

Total monthly expenses = $2124 + $200 = $2,324

After combing their expenses and incomes, the available amount that can be used to repay their new home loan is $4,920 (the monthly net income minus the net expenses)

Under previous serviceability test rate (7.2%), they can borrow $724K. But with the rate easing to 6.45%, they can borrow $782k from ASB. First home buyers like Tony and his wife are seeing their borrowing power increase by as much $;60k nearly.

(2) How does Bank of China (BOC) calculate their borrowing power? And how much more can they afford to borrow with a lower test rate?

If you deal with different lenders, you will get different loan amounts. When Bank of China calculate how much Tony and his wife can afford to borrow, they apply the different calculating model. The difference mainly comes from:

- Monthly net boarder income – Bank of China are happy to take two boarder income, and they take 100% (not like ASB taking discount). That’s why Tony’s monthly boarder income is much higher ($1,733) from the view of BOC

- Living expenses – the calculation from Bank of China ($2,200) is just slightly higher than ASB

So, from the perspective of Bank of China, the amount that can be used to repay Tony’s new home loan ($1,170) is higher than ASB

What we want to point out is, compared with the borrowing power ($989k) under the previous serviceability test rate (6.25%), now they can afford to borrow as much high as $113k - $145k more than they could before.

It’s important to note that your borrowing power will vary between lenders. If you get an offer from one lender, it does not mean you'll get a similar amount from the other, and it could have a massive difference like in this case.

3. Other factors affecting serviceability - how much mortgage you can afford

From the above case, you have understood how the serviceability test rate can affect your home loan borrowing power in a huge way. Apart from the test rate, here are some other factors that have big impact when working out your serviceability:

(1) Existing home loan

Mortgage lenders will take all your existing home loan into account when deciding whether you are eligible for a mortgage and how much you can afford to borrow. They’ll look at details of your existing loan, such as the current mortgage rates you’re repaying, the loan maturity dates, the repayment method (principal and interest, or interest only). So, if you improve the structure on your existing home loan, then it can make a huge difference on your future borrowing capacity.

(2) Living expenses

Banks use different methods to calculate your living expenses. With that saying, the calculation for the same case may vary between different banks.

(3) Boarder income

Some banks only allow a maximum of $150 - $200 per week to be used to pay a mortgage. Even though in some cities, it is easy to get more than that as rent. But banks don’t want to assume the very best-case scenario, they want to cap the amount to see if you can afford a mortgage. However, some banks do not set a cap amount. Also, some banks only consider one boarder income, regardless of how many spare bedrooms you have, while other banks allow two boarders.

So, not all lenders have the same serviceability assessment and apply the same test rate. It’s all about choosing the lender that suits your needs and situation best, and improving your existing home loan structure, then you may dramatically improve your borrowing power.

4. Is it much harder to get a home loan now (post Covid-19)?

Thinking about applying for a new loan during the post Covid-19? Some people comment it is harder to get a mortgage since the Covid-19. Our view is:

Yes, after Covid-19, banks have tightened up their lending policy, specifically regarding your income.

- If you are self-employed and your business just recovered from Covid-19, then it is probably too early for the bank to get comfort around your outgoing income.

- If you have recently moved into a new job for less than three months, then some banks may not consider your job as stable income until six months.

- If currently you don’t receive any rental income, maybe your parents are living in your property, or maybe your tenants just leave, then banks may not happy to use a rental appraisal because Covid-19 has caused New Zealand rental property market to fluctuate. We’ve seen the rent has reduced in some parts of New Zealand.

However, if your income is stable and you can prove your incomes, then in our view your borrowing capacity is increasing now. You can afford to borrow more than you could before.

5. How can I improve my home loan serviceability?

If you are looking to borrow money to buy a property and you have enough deposit or equity in your existing property, then your serviceability determines how much you can borrow. The followings are some of our recommendations:

First, you need to engage with an experienced and responsible mortgage advisor as early as possible. Do not wait until you find your dream property and plan to buy within a few days, then it is too late.

At Prosperity Finance, we don’t have a one-size-fits-all solution for your home loan. We look at your individual case, understand your needs and situation then make a tailored solution for you. That’s why it takes much time for us to do the preparation work, including:

- Does your existing home loan structure work well for you?

- Have you moved the equity to the bank that can lend you the most, so that you can borrow more to buy your next property?

- When it comes to home loan re-fix or refinance, it's important to think about your plan so that we know how long you should fix for and whether or not you should consider refinancing, etc.

6. The secret revealed: exposing the serviceability test rates that New Zealand banks are using to assess your home loan application (updating on July 2020)

Do you want to know the test rate your bank use? Here we reveal some of them, then it gives you the indication of what levels of the rates they are using to assess your application.

ANZ 6.65%

ASB 6.45%

BNZ 6.75%

Westpac 7.25%

Bank of China 5.0%

and we expect that more banks are considering reducing their test rates soon.

Prosperity Finance – here to help

We can assess your situation for free and give you an indication of how much you can afford to borrow. Call us at 09 930 8999 for a no-obligation chat with our adviser.

Other Blogs You Might Like:

LVR restriction removed and what does it mean for you?

Top 5 reasons your home loan application is declined and what you need to avoid

Incorrectly converting home to investment property could cost you extra $7k a year

Disclaimer: The content in this article are provided for general situation purpose only. To the extent that any such information, opinions, views and recommendations constitute advice, they do not take into account any person’s particular financial situation or goals and, accordingly, do not constitute personalised financial advice. We therefore recommend that you seek advice from your adviser before taking any action.

Archive

- April 2026 (1)

- February 2026 (1)

- December 2025 (1)

- October 2025 (1)

- August 2025 (2)

- July 2025 (1)

- June 2025 (2)

- April 2025 (1)

- October 2024 (1)

- July 2024 (1)

- June 2024 (1)

- April 2024 (1)

- January 2024 (1)

- December 2023 (1)

- November 2023 (3)

- October 2023 (3)

- September 2023 (3)

- August 2023 (2)

- July 2023 (4)

- June 2023 (2)

- May 2023 (5)

- April 2023 (4)

- March 2023 (2)

- February 2023 (3)

- November 2022 (4)

- October 2022 (1)

- September 2022 (2)

- August 2022 (1)

- July 2022 (4)

- June 2022 (2)

- April 2022 (1)

- March 2022 (3)

- February 2022 (1)

- December 2021 (3)

- November 2021 (3)

- October 2021 (3)

- September 2021 (3)

- August 2021 (2)

- July 2021 (2)

- June 2021 (2)

- May 2021 (3)

- April 2021 (3)

- March 2021 (3)

- February 2021 (4)

- January 2021 (3)

- December 2020 (3)

- November 2020 (4)

- October 2020 (3)

- September 2020 (2)

- August 2020 (2)

- July 2020 (5)

- June 2020 (3)

- May 2020 (3)

- April 2020 (4)

- March 2020 (4)

- February 2020 (3)

- January 2020 (3)

- December 2019 (1)

- November 2019 (4)

- October 2019 (5)

- September 2019 (4)

- August 2019 (4)

- July 2019 (5)

- June 2019 (4)

- May 2019 (5)

- April 2019 (3)

- March 2019 (5)

- February 2019 (3)

- January 2019 (1)

- November 2018 (1)

- October 2018 (1)

- January 2018 (4)