LVR restriction removed and what does it mean for you?

Posted by: Connie in Finance 101

On 30th April 2020, the New Zealand Reserve Bank has announced to remove mortgage loan-to-value ratio (LVR) restriction. This change marks the end of LVR limits and banks don’t need to comply with the LVR rule for the next 12 months at least.

After the announcement of this big change, we have been receiving a flood of enquiries asking us “how much more can I borrow now?” That’s why we’ll share with you how banks response since the LVR restriction removal and the possible impacts of the LVR lift in our view.

LVR restriction removed and what's the impact?

What has changed now since the LVR restrictions have been removed?

So far, main banks haven’t taken any action yet. We think it’s because:

In the current climate of Covid-19, people's income is not stable. In some cases, some of them have been reduced, which means banks have already exposed to the higher risks than ever. If they increase LVR, it will actually increase the risk even further. The timing probably is not ready in our view.

What’s more, this is a major policy change and applies to lending in a big way. All lenders will be considering how to adapt to the new rules and how to adjust their policies, which will absolutely take time. That’s the reasons why banks haven’t made any change yet. As always, we will give you a prompt update and share with you how the change applies to you.

Will the flood gates open? While the Reserve Bank removed the restriction on LVR, it does not necessarily mean banks won’t have their LVR rules. In our view, banks will not completely forgive deposits. Otherwise there will be more bad debts. That because if banks lend 100% of the purchase price, then banks are unlikely to recover their money in a case that the property has to go through mortgagee sale. We think they will eventually relax the LVR rules instead.

What is the impact of LVR removal? How much more can you borrow?

If the banks take actions to relax their LVR rules a bit, how that going to impact your borrowing capacity?

Firstly, you’ll need to understand how borrowing capacity is actually driven by two important factors – income capacity and deposit capacity

Income Capacity

The borrowing capacity coming from your income is called servicing. It stands for your repayment ability. In other words, how much disposal income do you have to service the loan.

The income that banks can consider includes:

- Your job income

- Your business income

- Your rental income coming from your investment properties or the borders at home

- Subsidy from government (e.g. Family Tax Credit)

If you don’t have enough disposable income to repay your home loan, banks won’t lend you the money because they have to follow a Responsible Lending Code – banks can only lend to customers who can demonstrate their ability to repay the home loans.

Deposit / LVR Capacity

Let’s say you have $200K deposit and LVR for first home buyer is 80%. This means banks only required 20% deposit and, in this case, you can borrow 800K to buy a million-dollar home because you have 20% deposit. When your deposit increase, or LVR changes, it will increase your borrowing power.

When New Zealand lenders calculate how much you can borrow for your home loan, they will consider both your income and the deposit you have, and then only factor in whichever is weaker.

If your deposit side is weaker compared to your servicing, then you can borrow more when the bank actually increases the LVR.

On the other hand, if the servicing side by your income is weaker than the LVR capacity, then your borrowing power won’t change, no matter how banks lift their LVR rules.

Illustrating the impact of LVR lift with two scenarios

Scenario 1: when your income side is weaker

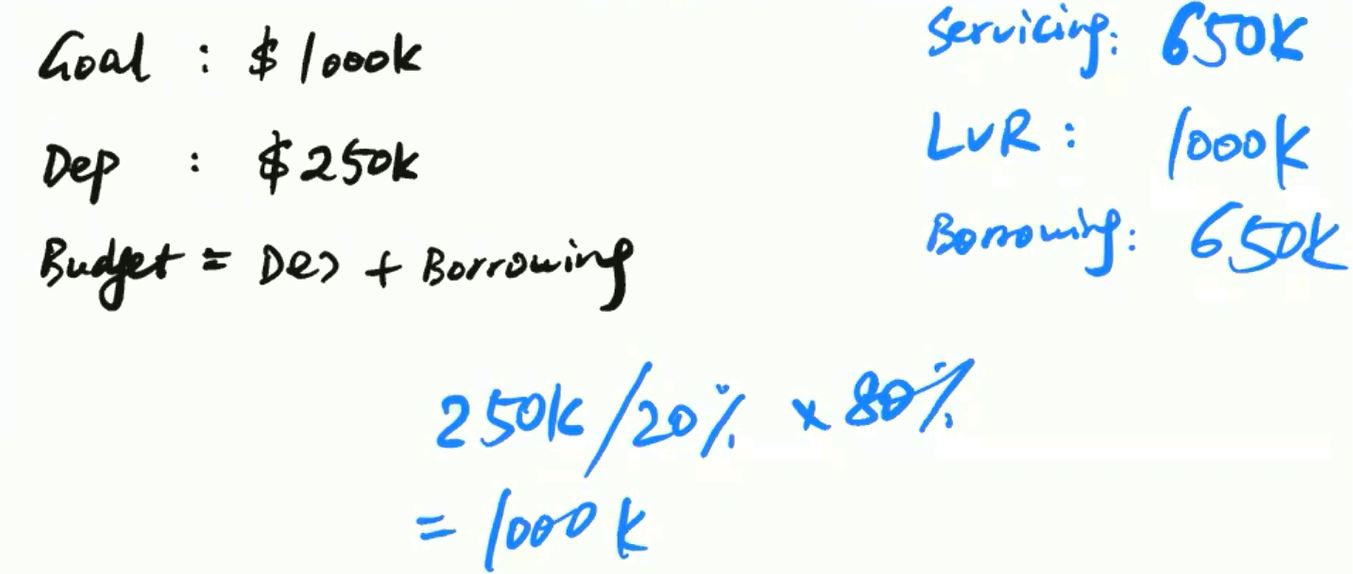

Let's say you want to buy a million-dollar home, and you have $250K deposit. Now you're looking to borrow $750K.

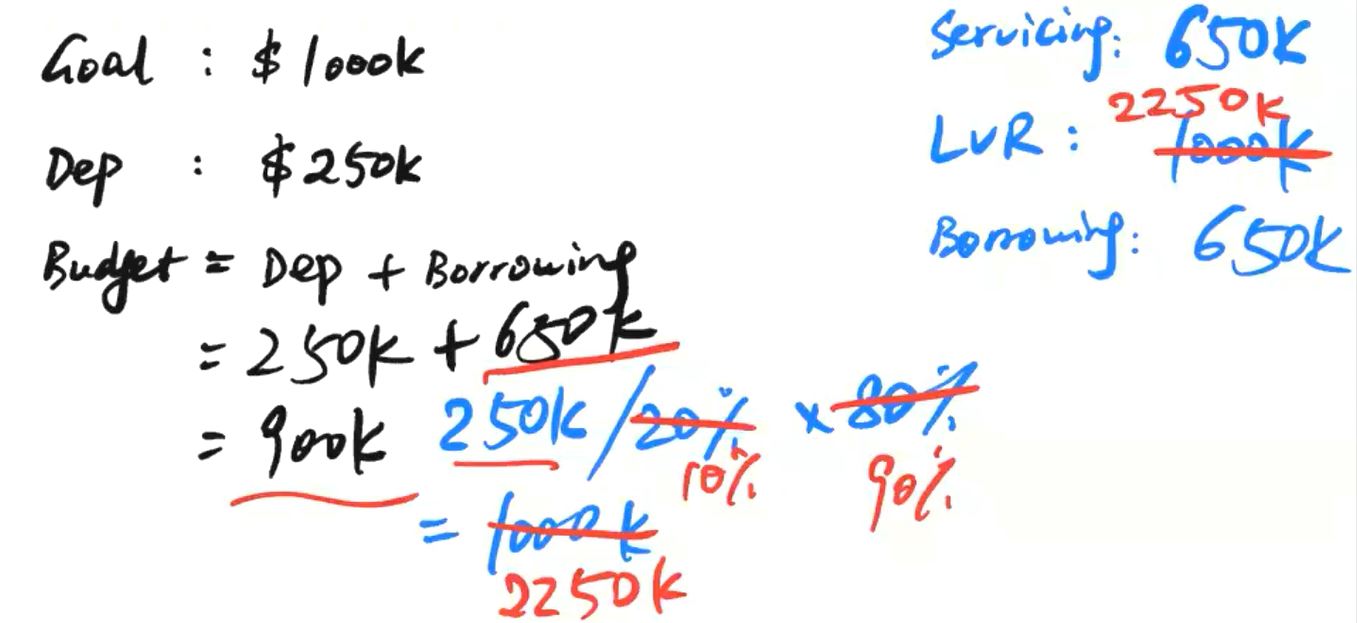

Say your income can allow you to service the loan of $650K. As you have $250K deposit and currently bank requires 20% deposit, your LVR capacity is one million dollars ($250K/20%*80%). Your servicing is weaker than your LVR capacity, so your borrowing power is based on the servicing ($650K). Even though you have more than enough deposits, the bank won't lend you more because you can only service 650K. So, your budget is $900k ($250k + $650k)

However, if the LVR can increase from 80% to 90%, what does it mean to your borrowing power?

After re-calculation, your LVR capacity increases to $2.25 million ($250K/10%*90%). As your servicing keeps the same ($650K) and is still weaker, so the borrowing capacity is still $650K.

So, in the case of servicing is weaker than the LVR sider, your borrowing power won’t make any change when the LVR increases or decreases.

Scenario 2: when your deposit side is weaker

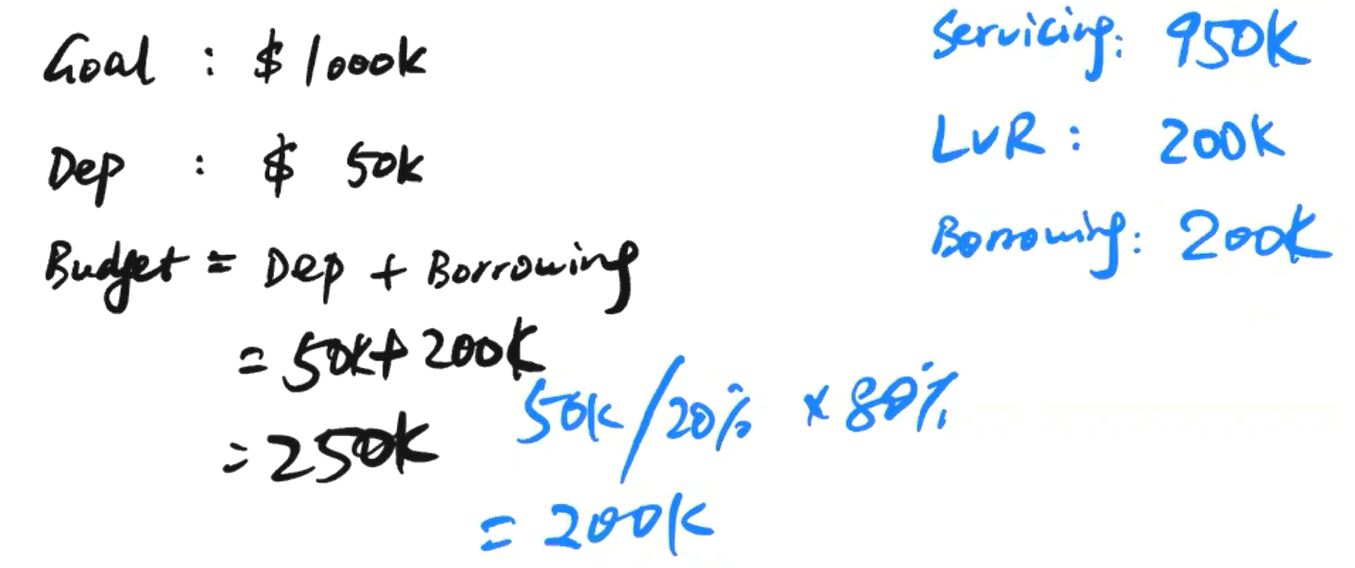

You’re also looking to buy a million-dollar home, but you only have 50K deposit

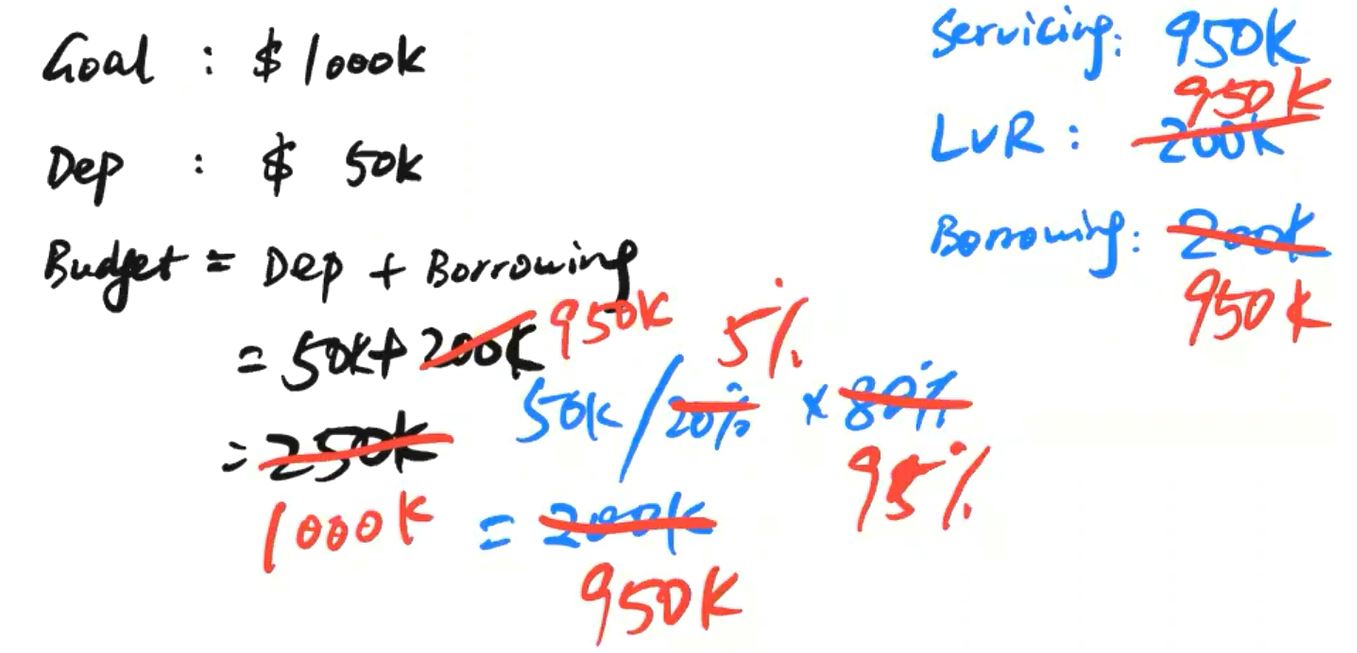

Say your income can afford the loan of $950K. Your LVR capacity is $200k ($50k/20%*80%). In this situation, even though you have high income, but limited to the deposit you have, your actual borrowing power narrows down to $200k. Then your house hunting will be very difficult within the budget of $250k.

However, what if the LVR increases to 95%, and only 5% of deposit is required. Then your LVR capacity significantly goes up to $950k ($50k/5%*95%). Considering the actual borrowing power will be the lower of the two, and in this case they are the same, $950k. Now, your choice of house hunting will be much wider within the budget of a million dollar.

As you can see from the above two examples, only when your LVR side of capacity is weaker than your serviceability, then you can borrow much more than ever if banks increase LVR. Otherwise, it won’t make any change.

Prosperity Finance – here to help

If you’d like to know how the LVR change will impact your borrowing power, and whether you can borrow much more than ever, then we are happy to provide you with a personalized solution that helps you unlock the potential, we’re professional mortgage broker and are here to help you. Call us at 09 930 8999 for a no-obligation chat with our adviser.

Read Further:

Reserve Bank proposes to remove the LVR restrictions?

Top 5 reasons your home loan application is declined and what you need to avoid

Loan to value ratio (LVR) restrictions for investment property return to 70%

Disclaimer: The content in this article are provided for general situation purpose only. To the extent that any such information, opinions, views and recommendations constitute advice, they do not take into account any person’s particular financial situation or goals and, accordingly, do not constitute personalised financial advice. We therefore recommend that you seek advice from your adviser before taking any action.

On 30th April 2020, the New Zealand Reserve Bank has announced to remove mortgage loan-to-value ratio (LVR) restriction. This change marks the end of LVR limits and banks don’t need to comply with the LVR rule for the next 12 months at least.

After the announcement of this big change, we have been receiving a flood of enquiries asking us “how much more can I borrow now?” That’s why we’ll share with you how banks response since the LVR restriction removal and the possible impacts of the LVR lift in our view.

LVR restriction removed and what's the impact?

What has changed now since the LVR restrictions have been removed?

So far, main banks haven’t taken any action yet. We think it’s because:

In the current climate of Covid-19, people's income is not stable. In some cases, some of them have been reduced, which means banks have already exposed to the higher risks than ever. If they increase LVR, it will actually increase the risk even further. The timing probably is not ready in our view.

What’s more, this is a major policy change and applies to lending in a big way. All lenders will be considering how to adapt to the new rules and how to adjust their policies, which will absolutely take time. That’s the reasons why banks haven’t made any change yet. As always, we will give you a prompt update and share with you how the change applies to you.

Will the flood gates open? While the Reserve Bank removed the restriction on LVR, it does not necessarily mean banks won’t have their LVR rules. In our view, banks will not completely forgive deposits. Otherwise there will be more bad debts. That because if banks lend 100% of the purchase price, then banks are unlikely to recover their money in a case that the property has to go through mortgagee sale. We think they will eventually relax the LVR rules instead.

What is the impact of LVR removal? How much more can you borrow?

If the banks take actions to relax their LVR rules a bit, how that going to impact your borrowing capacity?

Firstly, you’ll need to understand how borrowing capacity is actually driven by two important factors – income capacity and deposit capacity

Income Capacity

The borrowing capacity coming from your income is called servicing. It stands for your repayment ability. In other words, how much disposal income do you have to service the loan.

The income that banks can consider includes:

- Your job income

- Your business income

- Your rental income coming from your investment properties or the borders at home

- Subsidy from government (e.g. Family Tax Credit)

If you don’t have enough disposable income to repay your home loan, banks won’t lend you the money because they have to follow a Responsible Lending Code – banks can only lend to customers who can demonstrate their ability to repay the home loans.

Deposit / LVR Capacity

Let’s say you have $200K deposit and LVR for first home buyer is 80%. This means banks only required 20% deposit and, in this case, you can borrow 800K to buy a million-dollar home because you have 20% deposit. When your deposit increase, or LVR changes, it will increase your borrowing power.

When New Zealand lenders calculate how much you can borrow for your home loan, they will consider both your income and the deposit you have, and then only factor in whichever is weaker.

If your deposit side is weaker compared to your servicing, then you can borrow more when the bank actually increases the LVR.

On the other hand, if the servicing side by your income is weaker than the LVR capacity, then your borrowing power won’t change, no matter how banks lift their LVR rules.

Illustrating the impact of LVR lift with two scenarios

Scenario 1: when your income side is weaker

Let's say you want to buy a million-dollar home, and you have $250K deposit. Now you're looking to borrow $750K.

Say your income can allow you to service the loan of $650K. As you have $250K deposit and currently bank requires 20% deposit, your LVR capacity is one million dollars ($250K/20%*80%). Your servicing is weaker than your LVR capacity, so your borrowing power is based on the servicing ($650K). Even though you have more than enough deposits, the bank won't lend you more because you can only service 650K. So, your budget is $900k ($250k + $650k)

However, if the LVR can increase from 80% to 90%, what does it mean to your borrowing power?

After re-calculation, your LVR capacity increases to $2.25 million ($250K/10%*90%). As your servicing keeps the same ($650K) and is still weaker, so the borrowing capacity is still $650K.

So, in the case of servicing is weaker than the LVR sider, your borrowing power won’t make any change when the LVR increases or decreases.

Scenario 2: when your deposit side is weaker

You’re also looking to buy a million-dollar home, but you only have 50K deposit

Say your income can afford the loan of $950K. Your LVR capacity is $200k ($50k/20%*80%). In this situation, even though you have high income, but limited to the deposit you have, your actual borrowing power narrows down to $200k. Then your house hunting will be very difficult within the budget of $250k.

However, what if the LVR increases to 95%, and only 5% of deposit is required. Then your LVR capacity significantly goes up to $950k ($50k/5%*95%). Considering the actual borrowing power will be the lower of the two, and in this case they are the same, $950k. Now, your choice of house hunting will be much wider within the budget of a million dollar.

As you can see from the above two examples, only when your LVR side of capacity is weaker than your serviceability, then you can borrow much more than ever if banks increase LVR. Otherwise, it won’t make any change.

Prosperity Finance – here to help

If you’d like to know how the LVR change will impact your borrowing power, and whether you can borrow much more than ever, then we are happy to provide you with a personalized solution that helps you unlock the potential, we’re professional mortgage broker and are here to help you. Call us at 09 930 8999 for a no-obligation chat with our adviser.

Read Further:

Reserve Bank proposes to remove the LVR restrictions?

Top 5 reasons your home loan application is declined and what you need to avoid

Loan to value ratio (LVR) restrictions for investment property return to 70%

Disclaimer: The content in this article are provided for general situation purpose only. To the extent that any such information, opinions, views and recommendations constitute advice, they do not take into account any person’s particular financial situation or goals and, accordingly, do not constitute personalised financial advice. We therefore recommend that you seek advice from your adviser before taking any action.

Archive

- April 2026 (1)

- February 2026 (1)

- December 2025 (1)

- October 2025 (1)

- August 2025 (2)

- July 2025 (1)

- June 2025 (2)

- April 2025 (1)

- October 2024 (1)

- July 2024 (1)

- June 2024 (1)

- April 2024 (1)

- January 2024 (1)

- December 2023 (1)

- November 2023 (3)

- October 2023 (3)

- September 2023 (3)

- August 2023 (2)

- July 2023 (4)

- June 2023 (2)

- May 2023 (5)

- April 2023 (4)

- March 2023 (2)

- February 2023 (3)

- November 2022 (4)

- October 2022 (1)

- September 2022 (2)

- August 2022 (1)

- July 2022 (4)

- June 2022 (2)

- April 2022 (1)

- March 2022 (3)

- February 2022 (1)

- December 2021 (3)

- November 2021 (3)

- October 2021 (3)

- September 2021 (3)

- August 2021 (2)

- July 2021 (2)

- June 2021 (2)

- May 2021 (3)

- April 2021 (3)

- March 2021 (3)

- February 2021 (4)

- January 2021 (3)

- December 2020 (3)

- November 2020 (4)

- October 2020 (3)

- September 2020 (2)

- August 2020 (2)

- July 2020 (5)

- June 2020 (3)

- May 2020 (3)

- April 2020 (4)

- March 2020 (4)

- February 2020 (3)

- January 2020 (3)

- December 2019 (1)

- November 2019 (4)

- October 2019 (5)

- September 2019 (4)

- August 2019 (4)

- July 2019 (5)

- June 2019 (4)

- May 2019 (5)

- April 2019 (3)

- March 2019 (5)

- February 2019 (3)

- January 2019 (1)

- November 2018 (1)

- October 2018 (1)

- January 2018 (4)