Should you be concerned about DTI (debt-to-income ratio)?

Posted by: Connie in Property Investing

New Zealand finance minister, Grant Robertson, has agreed “in-principle” to add debt-to-income ratio (DTI) to the Reserve Bank’s toolkit to ensure financial stability and help control house prices to a sustainable level.

The DTI tool will enable the Reserve Bank New Zealand (RBNZ) to restrict how much a person can borrow based on their income to a certain multiple, but until the time of writing (July 2021) has not received the sign-off from the government about more details (e.g., the exact limits, the effective date, how the incomes are measured). It is estimated that a DTI cap would take at least six months to finalise. More importantly, the Reserve Bank won’t necessarily require banks to implement the DTI until the right timing.

The debt-to-income ratios are likely to be the most effective measurement that can be deployed by the RBNZ to support the stability of banking system. However, the restrictions will affect property investors, particularly those who are looking to grow their portfolios.

It appears that the introduction of DTI is unnecessary in our view – New Zealand banks have already tightened up their lending policies, and some banks still use a test interest rate as high as 7.25% to test if borrowers have the ability to afford the loan (despite actual rates currently dropping to sub 2% now).

In fact, ASB bank (the only one at the time of writing) has already started using this weapon back to last year. It requests a maximum of seven times of debt-to-income ratio as an additional restriction. With that said, investors who only deal with ASB probably have already reached their borrowing ceiling.

In this video, we’re going to have a deep dive at the debt-to-income ratio – who will be impacted, to what extent will it affect you (illustrating by a case study), and what strategies available to you, so you can start reviewing and considering how you can minimize the impact.

DTI (debt-to-income ratio)

Video Timeline

1. Who will be impacted by the implementation of the debt-to-income ratio? 04:37

2. Case study: to what extent will the DTI affect investors? 06:10

3. What are the strategies available right now? 12:59

1. Who will be impacted by the implementation of the debt-to-income ratio?

The DTI limits will impact property investors most significantly while having a limited impact on first-home buyers. This is because if you just look to borrow money to buy a home, banks already used their servicing calculation to limit borrowing capacity, and it unlikely to breach the DTI. However, if you are an investor, and the DTI is set as seven times, it’s very likely that you are unable to borrow more.

In a nutshell, the DTI restrictions will affect investors who:

- Just start building their portfolios and look to buy more rental properties.

- Look to buy in the areas where the house prices are already very expensive, such as Auckland, Wellington, Queenstown, and Tauranga. The average prices probably reach a million or over, resulting in relatively low rental yields.

2. Case study: to what extent will the DTI affect investors?

Assumptions:

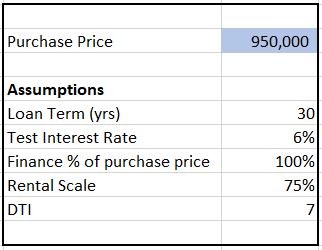

Let’s say you plan to purchase an investment property at the purchase price of $950,000, and there are some assumptions as follows:

- Loan term: 30 years

- Test interest rate: 6% (Currently, banks use test interest rates varying from 5.0% to 7.25% to calculate borrowing capacity)

- Finance percentage of purchase price: 100%. (In other words, borrow $950,000)

- Rental scale: 75%. (In case you're not familiar with how banks calculate your rental property income: Instead of requiring a copy of financial statements to verify your rental property income, banks calculate your rental income by a simple rule – only count a certain percentage (usually between 75 to 80% of your gross rental). They won't use 100% of your rental income because there are some costs involved in maintaining an investment property, such as insurance, rates, maintenance, and property management fee. Plus, banks also take the vacancy rate into consideration.)

- DTI: seven times.

(1) Let’s take a look at the servicing calculation used by banks at the moment:

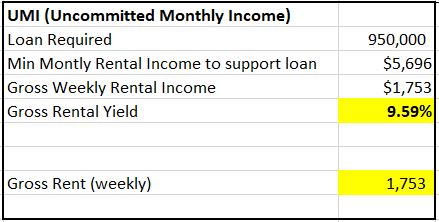

Currently, banks use what we call a UMI (Uncommitted Monthly Income) method to measure your borrowing capacity. It’s the dollar figure left over from net income after living costs and all home loan repayments. Usually banks allow a minimum UMI of $200-$300.

In this case of borrowing for $950,000, if you plan to only use the new rental income to fully cover the servicing requirements, the monthly net rent will need to reach $5,696, equivalent to $1,753 weekly gross income. This means the gross rental yield will need to be 9.59% - it seems impossible to have a rental yield as high as this, compared to the average level for the property worth $950,000 in Auckland sitting around 3.5%. So in order to borrow 100% to buy a rental property like this, you’ll need to have a high job income to supplement that.

That’s why investors could buy more properties in the past than they can today. Back a few years ago, New Zealand properties were less expensive, and the rent yield was higher. Also over the years, the rent increase was not at the same pace as the house price increase. So the debt servicing becomes weaker. As a result, it’s getting harder and harder to borrow. Plus, people who have a big portfolio normally wouldn’t just buy the rental and then rent it out. Instead, they actively do something to help add value to their properties such as renovation, adding another bedroom, or building another dwelling for example. As a result, both the property value and cashflow improve.

(2) What will happen when implementing DTI?

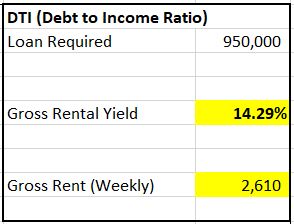

If DTI is introduced, in order to borrow for $950,000 in this case, you’ll need to have weekly gross rent of $2,610, which is equivalent to a gross rental yield of 14.29% - nearly impossible to achieve!

What can you expect once the DTI start implementing?

- If you look to borrow more to purchase a rental property, it’s nearly impossible.

- If you have an interest-only loan and it’s about coming to the end of term, you may not get the approval of extension for another few years because banks will do a full review on you, and they will consider the DTI if it is in place.

- If you want to partially discharge a property, your bank will do a full credit review. When the DTI is in place, the partial discharge can be an issue if the DTI test does not pass. (Note, a partial discharge means when you have more than one property that is secured by a loan, and you would like to release one of those properties as security, without repaying the full loan.

3. What are the strategies available right now?

There is no doubt that DTI will significantly impact property investors. However, from now, we would have at least six months before the DTI to finalise and (not guaranteed) implement. Instead of worrying about it, it’s better to take action now to minimise its impact. we’d recommend you act now:

(1) Buying rental properties as soon as you can

If you are thinking about buying more rental properties, we’d recommend acting now. Given that the current lending policies are not too tough, it’s still possible to buy an investment property along with the right structure and the right banks. Don’t wait until the DTI puts in place. It will be much harder for the servicing ability.

(2) Focusing on the cashflow

At the end of the day, the capital growth in the properties will help you substantially build your wealth. However, you need to have enough cashflow so that you can borrow more to buy properties.

One thing you can do is improving your job income. For example, if currently only a single-income earner in your family, then try to have two income earners. On the other hand, try to improve the cashflow by adding value or buying a property with a higher rental yield.

(3) Splitting banks

Having your properties secured with different banks, or what we call “splitting banks”, can help minimise the risk of enduring a negative lending policy. One thing for sure is that lending policies vary from one bank to another. In other words, if one bank introduces a lending policy that has an adverse impact on your borrowing capacity, you may still get a chance from the other bank. However, if you only stick with one bank, once their lending policy gets tougher, your borrowing capacity could reduce dramatically compared to the structure that you have property secured with different banks.

What’s more, when you have one property secured with one bank, there's no partial discharge issue because you simply pay off the loan for that particular property.

Prosperity Finance - Here to Help

In a net shell, you’d still have at least six months from now before the implementation of DTI. We highly recommend you taking action now. At Prosperity Finance, there's no one-size-fits-all approach. That’s why we welcome your enquiry so that we can make a tailored solution for you. Call us at 09 930 8999 to discuss your situation further.

Read more:

ANZ tightens servicing for rental property income, will this affect you?

Is it still a good time to invest in property?

New housing policy 2021: Can investors still afford to hold the properties they have?

Disclaimer: The content in this article are provided for general situation purpose only. To the extent that any such information, opinions, views and recommendations constitute advice, they do not take into account any person’s particular financial situation or goals and, accordingly, do not constitute personalised financial advice. We therefore recommend that you seek advice from your adviser before taking any action.

New Zealand finance minister, Grant Robertson, has agreed “in-principle” to add debt-to-income ratio (DTI) to the Reserve Bank’s toolkit to ensure financial stability and help control house prices to a sustainable level.

The DTI tool will enable the Reserve Bank New Zealand (RBNZ) to restrict how much a person can borrow based on their income to a certain multiple, but until the time of writing (July 2021) has not received the sign-off from the government about more details (e.g., the exact limits, the effective date, how the incomes are measured). It is estimated that a DTI cap would take at least six months to finalise. More importantly, the Reserve Bank won’t necessarily require banks to implement the DTI until the right timing.

The debt-to-income ratios are likely to be the most effective measurement that can be deployed by the RBNZ to support the stability of banking system. However, the restrictions will affect property investors, particularly those who are looking to grow their portfolios.

It appears that the introduction of DTI is unnecessary in our view – New Zealand banks have already tightened up their lending policies, and some banks still use a test interest rate as high as 7.25% to test if borrowers have the ability to afford the loan (despite actual rates currently dropping to sub 2% now).

In fact, ASB bank (the only one at the time of writing) has already started using this weapon back to last year. It requests a maximum of seven times of debt-to-income ratio as an additional restriction. With that said, investors who only deal with ASB probably have already reached their borrowing ceiling.

In this video, we’re going to have a deep dive at the debt-to-income ratio – who will be impacted, to what extent will it affect you (illustrating by a case study), and what strategies available to you, so you can start reviewing and considering how you can minimize the impact.

DTI (debt-to-income ratio)

Video Timeline

1. Who will be impacted by the implementation of the debt-to-income ratio? 04:37

2. Case study: to what extent will the DTI affect investors? 06:10

3. What are the strategies available right now? 12:59

1. Who will be impacted by the implementation of the debt-to-income ratio?

The DTI limits will impact property investors most significantly while having a limited impact on first-home buyers. This is because if you just look to borrow money to buy a home, banks already used their servicing calculation to limit borrowing capacity, and it unlikely to breach the DTI. However, if you are an investor, and the DTI is set as seven times, it’s very likely that you are unable to borrow more.

In a nutshell, the DTI restrictions will affect investors who:

- Just start building their portfolios and look to buy more rental properties.

- Look to buy in the areas where the house prices are already very expensive, such as Auckland, Wellington, Queenstown, and Tauranga. The average prices probably reach a million or over, resulting in relatively low rental yields.

2. Case study: to what extent will the DTI affect investors?

Assumptions:

Let’s say you plan to purchase an investment property at the purchase price of $950,000, and there are some assumptions as follows:

- Loan term: 30 years

- Test interest rate: 6% (Currently, banks use test interest rates varying from 5.0% to 7.25% to calculate borrowing capacity)

- Finance percentage of purchase price: 100%. (In other words, borrow $950,000)

- Rental scale: 75%. (In case you're not familiar with how banks calculate your rental property income: Instead of requiring a copy of financial statements to verify your rental property income, banks calculate your rental income by a simple rule – only count a certain percentage (usually between 75 to 80% of your gross rental). They won't use 100% of your rental income because there are some costs involved in maintaining an investment property, such as insurance, rates, maintenance, and property management fee. Plus, banks also take the vacancy rate into consideration.)

- DTI: seven times.

(1) Let’s take a look at the servicing calculation used by banks at the moment:

Currently, banks use what we call a UMI (Uncommitted Monthly Income) method to measure your borrowing capacity. It’s the dollar figure left over from net income after living costs and all home loan repayments. Usually banks allow a minimum UMI of $200-$300.

In this case of borrowing for $950,000, if you plan to only use the new rental income to fully cover the servicing requirements, the monthly net rent will need to reach $5,696, equivalent to $1,753 weekly gross income. This means the gross rental yield will need to be 9.59% - it seems impossible to have a rental yield as high as this, compared to the average level for the property worth $950,000 in Auckland sitting around 3.5%. So in order to borrow 100% to buy a rental property like this, you’ll need to have a high job income to supplement that.

That’s why investors could buy more properties in the past than they can today. Back a few years ago, New Zealand properties were less expensive, and the rent yield was higher. Also over the years, the rent increase was not at the same pace as the house price increase. So the debt servicing becomes weaker. As a result, it’s getting harder and harder to borrow. Plus, people who have a big portfolio normally wouldn’t just buy the rental and then rent it out. Instead, they actively do something to help add value to their properties such as renovation, adding another bedroom, or building another dwelling for example. As a result, both the property value and cashflow improve.

(2) What will happen when implementing DTI?

If DTI is introduced, in order to borrow for $950,000 in this case, you’ll need to have weekly gross rent of $2,610, which is equivalent to a gross rental yield of 14.29% - nearly impossible to achieve!

What can you expect once the DTI start implementing?

- If you look to borrow more to purchase a rental property, it’s nearly impossible.

- If you have an interest-only loan and it’s about coming to the end of term, you may not get the approval of extension for another few years because banks will do a full review on you, and they will consider the DTI if it is in place.

- If you want to partially discharge a property, your bank will do a full credit review. When the DTI is in place, the partial discharge can be an issue if the DTI test does not pass. (Note, a partial discharge means when you have more than one property that is secured by a loan, and you would like to release one of those properties as security, without repaying the full loan.

3. What are the strategies available right now?

There is no doubt that DTI will significantly impact property investors. However, from now, we would have at least six months before the DTI to finalise and (not guaranteed) implement. Instead of worrying about it, it’s better to take action now to minimise its impact. we’d recommend you act now:

(1) Buying rental properties as soon as you can

If you are thinking about buying more rental properties, we’d recommend acting now. Given that the current lending policies are not too tough, it’s still possible to buy an investment property along with the right structure and the right banks. Don’t wait until the DTI puts in place. It will be much harder for the servicing ability.

(2) Focusing on the cashflow

At the end of the day, the capital growth in the properties will help you substantially build your wealth. However, you need to have enough cashflow so that you can borrow more to buy properties.

One thing you can do is improving your job income. For example, if currently only a single-income earner in your family, then try to have two income earners. On the other hand, try to improve the cashflow by adding value or buying a property with a higher rental yield.

(3) Splitting banks

Having your properties secured with different banks, or what we call “splitting banks”, can help minimise the risk of enduring a negative lending policy. One thing for sure is that lending policies vary from one bank to another. In other words, if one bank introduces a lending policy that has an adverse impact on your borrowing capacity, you may still get a chance from the other bank. However, if you only stick with one bank, once their lending policy gets tougher, your borrowing capacity could reduce dramatically compared to the structure that you have property secured with different banks.

What’s more, when you have one property secured with one bank, there's no partial discharge issue because you simply pay off the loan for that particular property.

Prosperity Finance - Here to Help

In a net shell, you’d still have at least six months from now before the implementation of DTI. We highly recommend you taking action now. At Prosperity Finance, there's no one-size-fits-all approach. That’s why we welcome your enquiry so that we can make a tailored solution for you. Call us at 09 930 8999 to discuss your situation further.

Read more:

ANZ tightens servicing for rental property income, will this affect you?

Is it still a good time to invest in property?

New housing policy 2021: Can investors still afford to hold the properties they have?

Disclaimer: The content in this article are provided for general situation purpose only. To the extent that any such information, opinions, views and recommendations constitute advice, they do not take into account any person’s particular financial situation or goals and, accordingly, do not constitute personalised financial advice. We therefore recommend that you seek advice from your adviser before taking any action.

Archive

- April 2026 (1)

- February 2026 (1)

- December 2025 (1)

- October 2025 (1)

- August 2025 (2)

- July 2025 (1)

- June 2025 (2)

- April 2025 (1)

- October 2024 (1)

- July 2024 (1)

- June 2024 (1)

- April 2024 (1)

- January 2024 (1)

- December 2023 (1)

- November 2023 (3)

- October 2023 (3)

- September 2023 (3)

- August 2023 (2)

- July 2023 (4)

- June 2023 (2)

- May 2023 (5)

- April 2023 (4)

- March 2023 (2)

- February 2023 (3)

- November 2022 (4)

- October 2022 (1)

- September 2022 (2)

- August 2022 (1)

- July 2022 (4)

- June 2022 (2)

- April 2022 (1)

- March 2022 (3)

- February 2022 (1)

- December 2021 (3)

- November 2021 (3)

- October 2021 (3)

- September 2021 (3)

- August 2021 (2)

- July 2021 (2)

- June 2021 (2)

- May 2021 (3)

- April 2021 (3)

- March 2021 (3)

- February 2021 (4)

- January 2021 (3)

- December 2020 (3)

- November 2020 (4)

- October 2020 (3)

- September 2020 (2)

- August 2020 (2)

- July 2020 (5)

- June 2020 (3)

- May 2020 (3)

- April 2020 (4)

- March 2020 (4)

- February 2020 (3)

- January 2020 (3)

- December 2019 (1)

- November 2019 (4)

- October 2019 (5)

- September 2019 (4)

- August 2019 (4)

- July 2019 (5)

- June 2019 (4)

- May 2019 (5)

- April 2019 (3)

- March 2019 (5)

- February 2019 (3)

- January 2019 (1)

- November 2018 (1)

- October 2018 (1)

- January 2018 (4)