Do you have multiple properties secured with the same bank?

Posted by: Connie in Property Investing

It is very common to see that some people borrow money from the same bank when they purchase two or more properties.

Lenders will allow you to access your equity which you can then use to put down as deposit on another property – rather than take years to save.

However, when you have multiple properties secured with the same bank, by default, they will interlink all of your properties for added security. The more properties they hold as security, the safer they feel.

This is known as cross collateralisation: when more than one property is used to secure your loan by one lender. So why might this not be a good idea?

Do you have multiple properties secured with one bank?

Video Timeline:

Risk 1 - Their family home is exposed to your investment debt - 01:09

Risk 2 - Their sale proceeds could be at risk - 03:10

Risk 3 - They may be vulnerable to borrowing capacity glass ceilings - 04:30

Risk 4 - Exposed to interest rate rises - 05:24

Check out this case study:

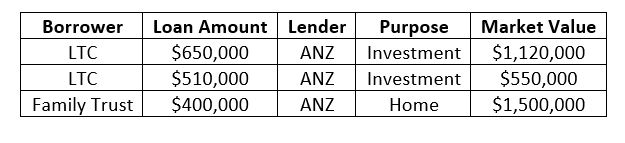

Mark and Jane, a married couple, have one home and two investment properties with the combined loan amount of $1,560,000.

Before the clients approached us, they faced several risks:

Risk 1 - Their family home is exposed to your investment debt.

In this case, their family home was cross-secured with their other investment properties.

This is risky. If you can’t repay your investment loans, your home is at risk because your lender has power over all your assets. They can decide to mortgagee sale your assets with full control over the sale proceeds, deciding which loan is to be repaid and by how much. You could even be forced to sell your family home in order to recover the remaining loan. These risks are unnecessary as you can still leverage property equity without the cross-securitisation structure.

After we analysed their situation, we moved one investment property loan over to ASB so that each investment property was secured by different banks. We also moved their family home to Westpac.

Risk 2 - Their sale proceeds could be at risk

If they wanted to sell any of their properties, ANZ would review whether their borrowing capacity and their equity level on the remaining securities was sufficient – giving Mark and Jane no control over the net sale proceeds.

If your lender takes full control over your property security, should you sell down one of your investments they can decide how much you need to repay from the sale proceeds.

We’ve seen clients who were forced to pay back full net proceeds to their lender – with nothing left for themselves. If you only have one property with one lender, you simply pay off the entire loan and keep the remaining net sale proceeds.

Risk 3 – They may be vulnerable to borrowing capacity glass ceilings

They wanted to buy another investment property, and they went back to their bank ANZ. Unfortunately, ANZ told them further borrowing was not possible.

In this case, although ANZ refused further borrowing for another investment property, we were able to secure an approval from Bank of China for the maximum LVR of 70% of the purchase price, with the remaining 30% topped up from Westpac against their family home. This allowed Mark and Jane to use the equity gained from their family home as a deposit whilst keeping their family home well away from any investment property lenders.

This is because not all lenders are equal. The borrowing capacity can widely vary from one lender to another simply due to different servicing calculation policies. The gap between lenders is getting bigger and bigger with some lending up to 3 times more than another bank. If you spread your properties across multiple lenders, should any of them change or tighten their lending criteria it’s easier to switch out to another lender.

Risk 4 - Exposed to interest rate rises

If ANZ’s interest rates were just 0.2% higher than other banks, they would have to pay around an extra $3,000 in interest costs p.a. – compared with significant savings borrowing from another bank.

When your loan comes off a fixed term and needs re-fixing, you may not be happy with the interest rates your current bank is offering and wish to switch to another lender. However, if personal circumstances or bank policies do not allow this, you potentially face significant rate increases. They may not allow you to extend your interest-only term, therefore you have to pay the principles and interests. The bigger the loan with one single lender, the more vulnerable you become. In a worst-case scenario, you may have to sell down some of your properties to reduce the loan repayment pressure.

What’s more, if you have several interest-only loans with one bank and your interest-only terms are about to end, you will endure the pressure of repaying a principal and interest loan. It could be risky for you if you have insufficient cash flow to pay the mortgage.

If you have two or more properties with one bank, before you go to your bank and borrow more money, we highly recommend you take time to review and see if you can split them with different banks.

Now, if you are not sure about the best loan structure, we are happy to offer a free, no obligation loan review for you, so that you can prevent the above scenarios from happening.

Disclaimer: The content in this article are provided for general situation purpose only. To the extent that any such information, opinions, views and recommendations constitute advice, they do not take into account any person’s particular financial situation or goals and, accordingly, do not constitute personalised financial advice. We therefore recommend that you seek advice from your adviser before taking any action.

Prosperity Finance – here to help

Prosperity Finance looks at your loans strategically, empowering you to make the best long-term, informed decisions. We are professional mortgage brokers and are here to help. Give us a call today on 09 930 8999.

Other Blogs You Might Like:

Your sale proceeds could be at risk when you hold multiple properties secured with one lender

Incorrectly converting home to investment property could cost you extra $7k a year

How much more mortgage can I afford? (Tips to quickly increase your borrowing power by 800k)

It is very common to see that some people borrow money from the same bank when they purchase two or more properties.

Lenders will allow you to access your equity which you can then use to put down as deposit on another property – rather than take years to save.

However, when you have multiple properties secured with the same bank, by default, they will interlink all of your properties for added security. The more properties they hold as security, the safer they feel.

This is known as cross collateralisation: when more than one property is used to secure your loan by one lender. So why might this not be a good idea?

Do you have multiple properties secured with one bank?

Video Timeline:

Risk 1 - Their family home is exposed to your investment debt - 01:09

Risk 2 - Their sale proceeds could be at risk - 03:10

Risk 3 - They may be vulnerable to borrowing capacity glass ceilings - 04:30

Risk 4 - Exposed to interest rate rises - 05:24

Check out this case study:

Mark and Jane, a married couple, have one home and two investment properties with the combined loan amount of $1,560,000.

Before the clients approached us, they faced several risks:

Risk 1 - Their family home is exposed to your investment debt.

In this case, their family home was cross-secured with their other investment properties.

This is risky. If you can’t repay your investment loans, your home is at risk because your lender has power over all your assets. They can decide to mortgagee sale your assets with full control over the sale proceeds, deciding which loan is to be repaid and by how much. You could even be forced to sell your family home in order to recover the remaining loan. These risks are unnecessary as you can still leverage property equity without the cross-securitisation structure.

After we analysed their situation, we moved one investment property loan over to ASB so that each investment property was secured by different banks. We also moved their family home to Westpac.

Risk 2 - Their sale proceeds could be at risk

If they wanted to sell any of their properties, ANZ would review whether their borrowing capacity and their equity level on the remaining securities was sufficient – giving Mark and Jane no control over the net sale proceeds.

If your lender takes full control over your property security, should you sell down one of your investments they can decide how much you need to repay from the sale proceeds.

We’ve seen clients who were forced to pay back full net proceeds to their lender – with nothing left for themselves. If you only have one property with one lender, you simply pay off the entire loan and keep the remaining net sale proceeds.

Risk 3 – They may be vulnerable to borrowing capacity glass ceilings

They wanted to buy another investment property, and they went back to their bank ANZ. Unfortunately, ANZ told them further borrowing was not possible.

In this case, although ANZ refused further borrowing for another investment property, we were able to secure an approval from Bank of China for the maximum LVR of 70% of the purchase price, with the remaining 30% topped up from Westpac against their family home. This allowed Mark and Jane to use the equity gained from their family home as a deposit whilst keeping their family home well away from any investment property lenders.

This is because not all lenders are equal. The borrowing capacity can widely vary from one lender to another simply due to different servicing calculation policies. The gap between lenders is getting bigger and bigger with some lending up to 3 times more than another bank. If you spread your properties across multiple lenders, should any of them change or tighten their lending criteria it’s easier to switch out to another lender.

Risk 4 - Exposed to interest rate rises

If ANZ’s interest rates were just 0.2% higher than other banks, they would have to pay around an extra $3,000 in interest costs p.a. – compared with significant savings borrowing from another bank.

When your loan comes off a fixed term and needs re-fixing, you may not be happy with the interest rates your current bank is offering and wish to switch to another lender. However, if personal circumstances or bank policies do not allow this, you potentially face significant rate increases. They may not allow you to extend your interest-only term, therefore you have to pay the principles and interests. The bigger the loan with one single lender, the more vulnerable you become. In a worst-case scenario, you may have to sell down some of your properties to reduce the loan repayment pressure.

What’s more, if you have several interest-only loans with one bank and your interest-only terms are about to end, you will endure the pressure of repaying a principal and interest loan. It could be risky for you if you have insufficient cash flow to pay the mortgage.

If you have two or more properties with one bank, before you go to your bank and borrow more money, we highly recommend you take time to review and see if you can split them with different banks.

Now, if you are not sure about the best loan structure, we are happy to offer a free, no obligation loan review for you, so that you can prevent the above scenarios from happening.

Disclaimer: The content in this article are provided for general situation purpose only. To the extent that any such information, opinions, views and recommendations constitute advice, they do not take into account any person’s particular financial situation or goals and, accordingly, do not constitute personalised financial advice. We therefore recommend that you seek advice from your adviser before taking any action.

Prosperity Finance – here to help

Prosperity Finance looks at your loans strategically, empowering you to make the best long-term, informed decisions. We are professional mortgage brokers and are here to help. Give us a call today on 09 930 8999.

Other Blogs You Might Like:

Your sale proceeds could be at risk when you hold multiple properties secured with one lender

Incorrectly converting home to investment property could cost you extra $7k a year

How much more mortgage can I afford? (Tips to quickly increase your borrowing power by 800k)

Archive

- April 2026 (1)

- February 2026 (1)

- December 2025 (1)

- October 2025 (1)

- August 2025 (2)

- July 2025 (1)

- June 2025 (2)

- April 2025 (1)

- October 2024 (1)

- July 2024 (1)

- June 2024 (1)

- April 2024 (1)

- January 2024 (1)

- December 2023 (1)

- November 2023 (3)

- October 2023 (3)

- September 2023 (3)

- August 2023 (2)

- July 2023 (4)

- June 2023 (2)

- May 2023 (5)

- April 2023 (4)

- March 2023 (2)

- February 2023 (3)

- November 2022 (4)

- October 2022 (1)

- September 2022 (2)

- August 2022 (1)

- July 2022 (4)

- June 2022 (2)

- April 2022 (1)

- March 2022 (3)

- February 2022 (1)

- December 2021 (3)

- November 2021 (3)

- October 2021 (3)

- September 2021 (3)

- August 2021 (2)

- July 2021 (2)

- June 2021 (2)

- May 2021 (3)

- April 2021 (3)

- March 2021 (3)

- February 2021 (4)

- January 2021 (3)

- December 2020 (3)

- November 2020 (4)

- October 2020 (3)

- September 2020 (2)

- August 2020 (2)

- July 2020 (5)

- June 2020 (3)

- May 2020 (3)

- April 2020 (4)

- March 2020 (4)

- February 2020 (3)

- January 2020 (3)

- December 2019 (1)

- November 2019 (4)

- October 2019 (5)

- September 2019 (4)

- August 2019 (4)

- July 2019 (5)

- June 2019 (4)

- May 2019 (5)

- April 2019 (3)

- March 2019 (5)

- February 2019 (3)

- January 2019 (1)

- November 2018 (1)

- October 2018 (1)

- January 2018 (4)